ShadowFall Disclaimer

Contact: [email protected]

Responsible for this content: Matthew Earl

ShadowFall Capital & Research LLP is authorised and regulated by the

Financial Conduct Authority.

ShadowFall Capital & Research LLP Important Information, Disclaimer and

Disclosures:

This website entry (“entry”), which contains an implicit research recommendation, has been produced by ShadowFall Capital & Research LLP (“ShadowFall”), which is authorised and regulated by the Financial Conduct Authority in the United Kingdom (firm reference number 782080). This entry has been produced exclusively by Matthew Earl who is the Managing Partner of ShadowFall at ShadowFall (the “author”). The content and information in this entry is provided to you subject to the terms below and those contained within ShadowFall’s Social Media Disclaimer, which must each be adhered to at all times.

This entry was completed and first distributed at 10 am GMT on Thursday 2 May 2019, and contains certain observations and opinions that have been previously issued to ShadowFall’s clients in a research report, which was completed and distributed at 5 pm GMT on Friday 31 August 2018. Unless otherwise specified, the information and opinions presented or contained in this entry are provided as of the date this document was written. ShadowFall is under no obligation to update, revise or affirm this entry.

ShadowFall has taken all reasonable steps to ensure that factual information in this entry is true and accurate. However, where such factual information is derived from publicly available sources ShadowFall has relied on the accuracy of those sources.

Some of the open source data contained in this report may have been sourced from public records made available by Companies House, which is licensed under the Open Government License; https://www.nationalarchives.gov.uk/doc/open-government-licence/version/3/

All statements of opinion contained in this entry are based on ShadowFall’s own assessment based on information available to it. That information may not be complete or exhaustive. No representation is made or warranty given as to the accuracy, completeness, achievability or reasonableness of such statements of opinion.

This entry is only intended for and will only be distributed to persons who qualify as FCA defined Professional Clients, who are expected to make their own judgment as to any reliance that they place on the contents of this entry. It is not suitable for, nor intended for any persons deemed to be a “Retail Client” under the FCA Rules. In addition, the content of this entry is not intended for any jurisdiction outside of which ShadowFall is not authorised.

ShadowFall does not take responsibility or accept any liability for any action taken or not taken by the recipient of this entry as a result of information and/or opinions contained in the entry. Recipients must exercise their own judgment and where appropriate take their own investment, tax and legal advice prior to taking or not taking action in reliance on any of the contents of this entry.

Forward-looking information or statements in this entry contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. ShadowFall makes no representation herein that forward-looking predictions shall come to pass.

Neither the author nor ShadowFall are aware of any factor, subject to the paragraph below, which might reasonably be expected to impair their objectivity in the preparation of this entry. The author and ShadowFall are not aware of any direct or indirect conflicts of interest, subject to the paragraph below, that might exist between the author or ShadowFall and any issuer which is the subject of this entry (the “issuers”). In particular, neither the author nor ShadowFall has any affiliation with the issuers.

ShadowFall manages an alternative investment fund (the “fund”) which inter alia takes positions in traded securities. At the time of distribution of this entry on 2 May 2019 the fund holds short positions in the issuers, which may include through options, swaps or other derivatives relating to the issuers. The fund may take further positions in the issuers (long or short) at a future date.

In addition, at the time of distribution of this entry, the author is invested in the fund.

ShadowFall is committed to providing services and products which are unbiased and impartial and have implemented a Conflicts of Interest Policy pursuant to FCA rules.

The existence and content of this entry has not been discussed in any way with the issuers or their corporate brokers prior to completion and publication. Neither the author nor ShadowFall has received any payment from the issuer, its corporate broker or any connected party for preparing this research report.

Prior to completion and distribution, this entry

has been seen by ShadowFall’s legal advisers and its regulatory advisers.

LATIN (AMERICA) AND CONCERNS OVER GUARANTEES, DEBT & CAPITALISATION.

A sagacious journalist for the Financial Times, Robert Smith, recently wrote an interesting [1] article on how ex ante[2] some Private Equity (PE) firms attempt to boost their target business’ numbers ahead of acquisition: Equivalent of doping? Private equity takes juicing the numbers to the next level.

Mr Smith writes:

Heavily adjusted earnings have become an inescapable fact of life in the modern buyout boom. Private equity firms now use eyebrow-raising “Pro-forma” earnings numbers, a useful bit of Latin allowing them to factor in cost savings before they are even made.

This has the helpful effect of bringing down a buyout’s leverage, the crucial measure of how much debt it has relative to its annual earnings.

It would seem that PE firms are banking targeted cost savings ahead of, or ex ante, such savings being achieved. The opposite path to take, and some may say more prudent approach, would be to base a buyout’s leverage on its existing costs and adjust that leverage after the event, or ex post[3], any cost savings being realised. This is a utilisation of Pro-forma[4] accounting. As we discuss below, its use is not limited to the PE market.

Another Latin phrase in the financial lexicon that one may wish to get to grips with is the term, Ultimo[5].

ARCADIS

Arcadis is a Dutch listed international engineering company, with a global presence in over 70 countries. The group specialises in design, consultancy, engineering, project and management services. It operates in four business lines: Buildings (41%), Infrastructure (25%), Environment (22%) and Water (12%). On a regional basis, the group’s revenues are split: Americas (31%), Europe and Middle East (46%) and Asia Pacific (14%), and CallisonRTKL (9%).

Arcadis

reported revenue of €3.3bn and a net loss of €26m to 31 December 2018.

ARCADIS: ULTIMO AND PRO-FORMA

Whilst itself sounding like a Latin word, Arcadis doesn’t appear to mean anything. However, Arcadis does use Latin in its financial statements. Notably the terms: Pro-forma and Ultimo.

For example, when reporting its:

EBITDA for debt covenant purposes, Arcadis seems to use a Pro-forma measure [6]. In our view, this is a subjective approach to defining EBITDA and not especially prudent.

Average Net Debt for debt covenant purposes, Arcadis appears to use a limited Ultimo period [7]. We interpret this to mean that it is the average in the last month of the Q2 and Q4, however, it may be as narrow a reporting point as the final day of each quarter.

The questions we have are:

- Is this an indication of aggressive accounting that we so often look for?

- If so, then in the light of our discussion on Short Sellers and Auditors, is Arcadis’ audit firm exercising sufficient professional scepticism?

On the basis that we see signs of issues elsewhere within Arcadis’ financial statements (some of which we discuss below), our concern is that the respective answers would be yes and no.

LATIN IS ONE THING; OFF-BALANCE SHEET GUARANTEES ARE ANOTHER

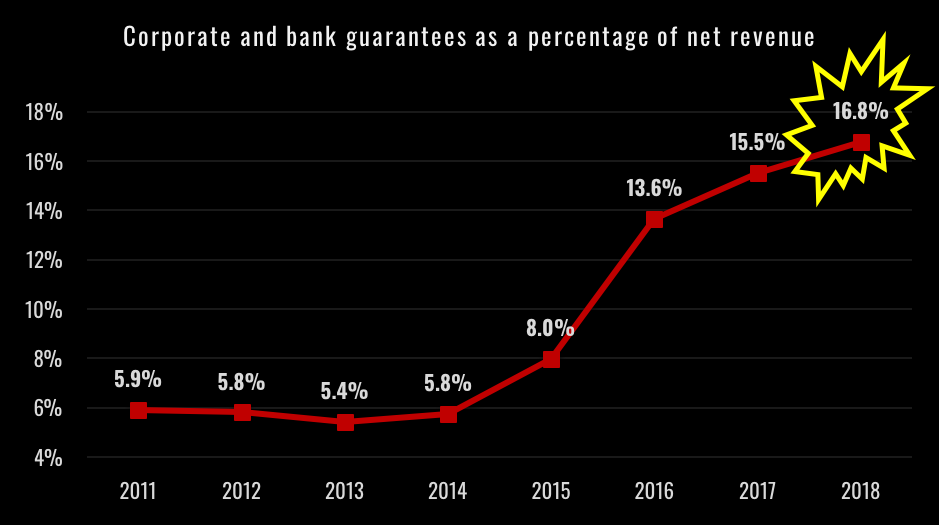

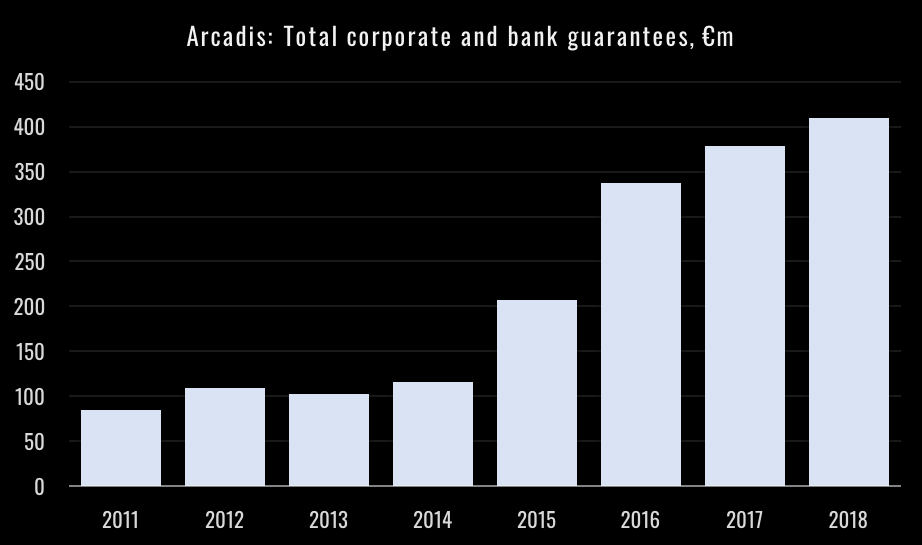

Over recent years Arcadis has reported a decline in its total loans and borrowings (debt). At the same time there has been significant growth in its off-balance sheet guarantees that are associated with corporate and bank guarantees (guarantees). In 2011, these guarantees stood at €85.3m. By 2018 these guarantees had grown to €409.5m as compared to on balance sheet borrowings of €588.2m.

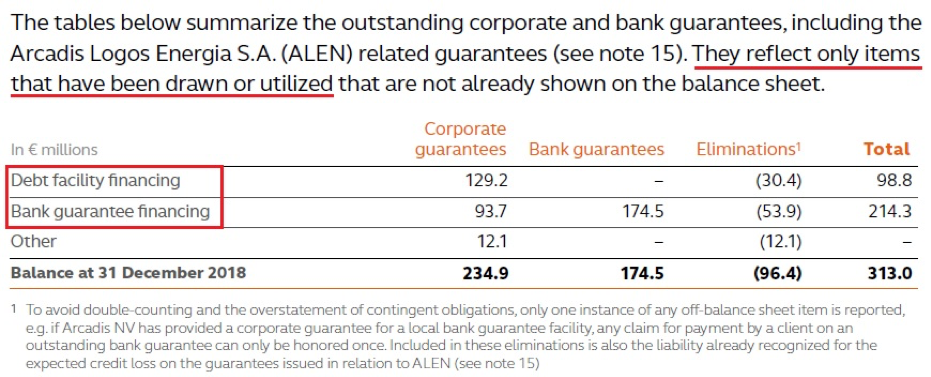

Arcadis’ management recently described these guarantees as largely relating to “performance guarantees on projects” with relatively small values of c. €100,000. However, in the case of its Brazilian JV, €87m in guarantees appears to relate entirely to the JV’s borrowing. Further, within its 2018 financial statements these guarantees are described as relating to “debt facility” or “bank guarantee” financing, that has either been “drawn or utilized”.

These guarantees equated to 16.8% of net revenue in 2018, as compared to 5.9% of net revenue in 2011. If project performance related, then this marked rise in use of guarantees might suggest that Arcadis has experienced a deterioration in its partners’ perception of its performance on projects. An alternative explanation is that these guarantees are as they are described in Arcadis’ filings and exemplified by its Brazilian JV, i.e. off-balance sheet guarantees relating to a growing stock of debt.

Were these guarantees to be brought onto Arcadis balance sheet, then we believe that Arcadis would be in breach of its debt covenant that requires net debt to EBITDA ratio to be less than 3.0x.

THE JV IN BRAZIL: ALEN

Arcadis’ Brazilian JV, Arcadis Logos Energia SA (ALEN), accounts for €87m in guarantees. However, if ALEN is an example of the quality and nature of these guarantees then, in our view, Arcadis’ creditors ignore these sizeable guarantees at their peril.

In the case of ALEN:

- Arcadis appears to have equity valued at ZERO as security for its guarantees, which begs the question, does it have security for its guarantees to other partners?

- Arcadis, in a somewhat circular manner, seems to guarantee its own loans to ALEN; is this common with guarantees to other partners?

- Not only does Arcadis guarantee loans to ALEN, it also guarantees loans to affiliates of ALEN. In 2018, these affiliate guarantees were €24m.

- When Arcadis impaired some of the ALEN loans it didn’t utilise the cross guarantees it had from its JV partners. Is this isolated to ALEN?

- Arcadis has apparently waived interest due on its ALEN shareholder loans, however, were further guarantees provided to ALEN so that it could service its external debt obligations? Does Arcadis service the debt facilities and bank guarantees of its other partners? Arcadis’ cash interest paid, compared to the weighted average interest rate it reports, we believe points to Arcadis servicing this off-balance sheet debt.

A JV IS FORMED

On 9 December 2011, Arcadis formed a Brazilian joint venture (JV) by selling 2 shares (or 50.01%) in its Brazilian energy business, ALEN. ALEN was then deconsolidated at year end.

The energy projects of ALEN consisted of biogas installations and hydropower plants. At the commencement of the ALEN JV, Arcadis detailed that the income from the assets was to be distributed according to the joint shareholding. However, as of 2018, any significant income has yet to arrive.

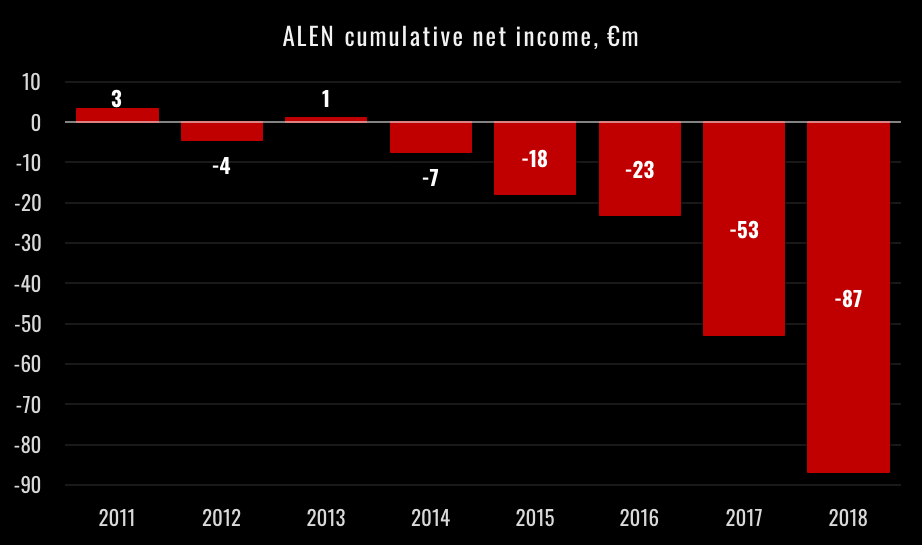

Since its deconsolidation we believe it’s fair to say that ALEN has performed poorly. ALEN reported a post-tax loss of €34.1m in 2018 (2017: €29.6m) bringing its cumulative losses to €86.9m since 2011.

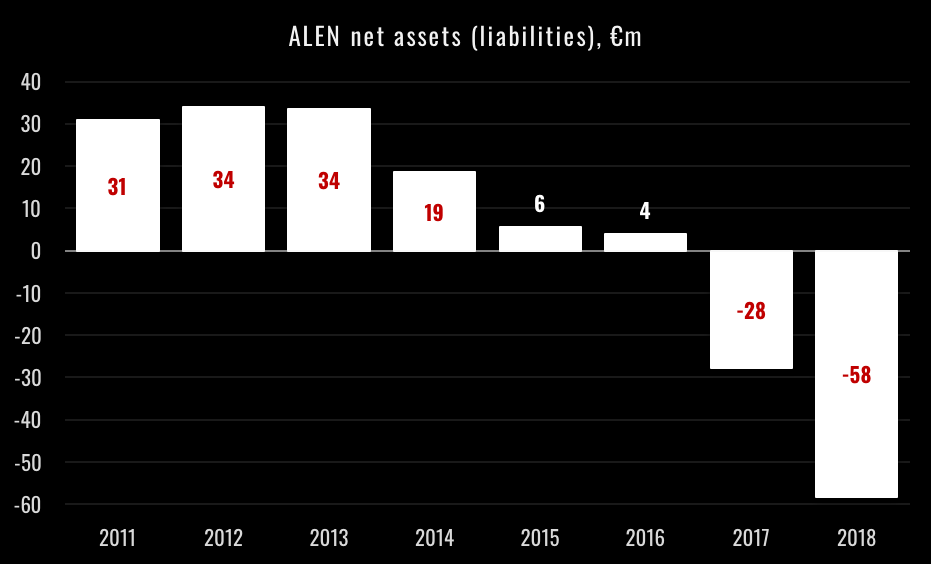

As of 31 December 2018, ALEN had net liabilities of €58.3m (2017: net liabilities of €27.7m). This compares to reported net assets of €30.9m in 2011.

GUARANTEEING ITS OWN LOANS?

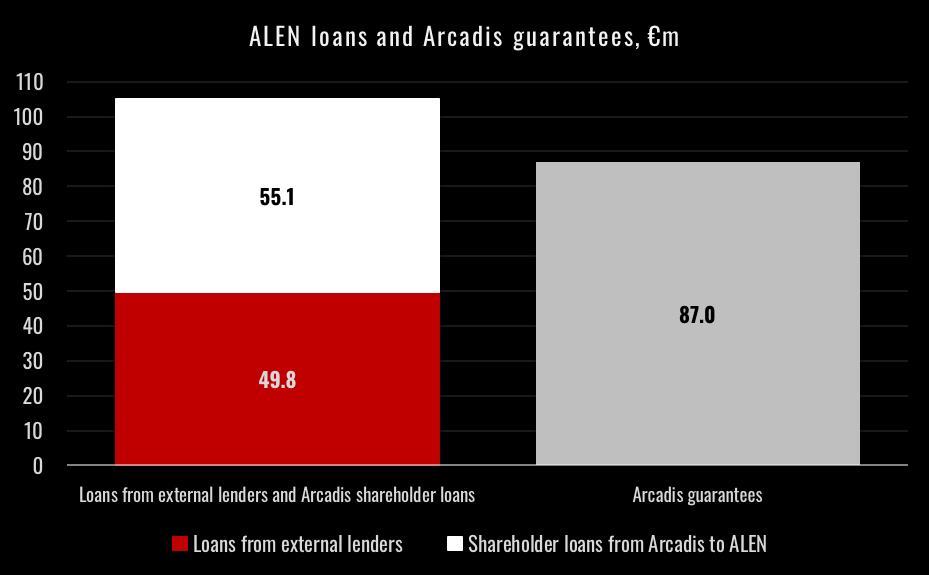

Arcadis reported it provided guarantees of €87m to ALEN in 2018 (2017: €84m).

In 2018, ALEN had:

- Net liabilities of €58.3m.

Of which:

- Current liabilities totalled €106.4m.

These current liabilities included:

- Loans from external lenders of €49.8m; and

- Shareholder loans from Arcadis to ALEN of €55.1m.

However, Arcadis highlights (our bold for emphasis) [8]:

The shareholders in ALEN, Logos Holding S.A. and Arcadis, provided corporate guarantees to the lenders of ALEN for loans to ALEN and its affiliates. The total amount of guarantees provided by Arcadis at 31 December 2018 was €87 million (2017: €84 million), of which €63 million was related to bank loans provided to ALEN (2017: €68 million) and €24 million to bank loans provided to affiliates of ALEN (2017: €16 million).

If ALEN has €49.8m in loans from external lenders and €55.1m in shareholder loans from Arcadis (€104.9m in total) and Arcadis is guaranteeing €87m in loans to ALEN and its affiliates, then this looks to us like Arcadis guarantees some or all of its own shareholder loans.

If Arcadis is guaranteeing its own loans to ALEN, then we view this as an altogether strange and somewhat circular state of affairs. An alternative explanation is that Arcadis is not guaranteeing its own loans to ALEN, however this might suggest that ALEN has further loans above the €49.8m from external lenders that account for the €87m in guarantees; i.e. an additional €37.2m in guaranteed loans.

LOANS TO AFFILIATES

In 2018, for the first time in its financial statements, Arcadis details the breakdown of the ALEN loans that are guaranteed and mentions that €24m (2017: €16m) of these loans are to ALEN affiliates. €24m in bank loans is a significant sum, and these are reportedly provided to affiliates of ALEN.

Some questions we would have are:

- Who are the affiliates?

- How are they affiliated to ALEN?

- Are they owned or co-owned either by Arcadis or ALEN?

- What has €24m been loaned for [9]?

- Why did the loans increase by a further €8m in 2018?

- Why is 2018 the first time there has been any mention of loans to ALEN affiliates within Arcadis’ financial statements [10]?

As for how these loans are described we note that Arcadis reports the guarantees as relating to €63m in bank loans to ALEN and €24m in bank loans to affiliates of ALEN. They key term here is bank loans.

If ALEN has loans from external lenders of €49.8m and shareholder loans from Arcadis of €55.1m, then presumably the latter is simply a loan from Arcadis and would not qualify as a bank loan? Whereas Arcadis reports a total of €87m in bank loans as being guaranteed as compared to €49.9m of loans from external lenders (presumably banks).

GUARANTEES WITH MEANINGLESS CROSS GUARANTEES?

With regards to the ALEN guarantees, in 2017, Arcadis reported (our bold for emphasis):

The Group provided guarantees to the lenders of ALEN for an amount of €84 million as at 31 December 2017. Arcadis is therefore exposed to the risk of ALEN (or an ALEN subsidiary) running into financial difficulty that might trigger a default on debt that would, in turn, result in the lender(s) claiming repayment from the Group. In return for the guarantees Arcadis received cross guarantees from the other shareholders.

The above states that although Arcadis had guaranteed the ALEN loans, it had “cross guarantees” from the other shareholders. One could easily be forgiven for thinking that these guarantees were monetary based. However, Arcadis’ 2018 financial statements appear to suggest that the cross guarantees have no cash backing and are guaranteed by equity in ALEN; an arrangement which we believe has its flaws.

We further note that within its 2018 financial statements, Arcadis highlights (our bold for emphasis):

In December 2018 the shareholder loans were transferred from Arcadis Logos S.A. to the corporate holding company that also owns the equity interest. At the same time the interest on the shareholder loans was reduced to nil, with the consent of ALEN, to stop accruing further interest payable in ALEN and related withholding taxes, as it is expected that ALEN will not be able to repay this to Arcadis in the future. The maturity dates of the loans were changed to December 2019.

Typically, in our view, if a company is unable to service its debt, then generally the equity of that company is approaching worthless. Arcadis goes on to state (our bold for emphasis):

Logos Holding S.A. [the ALEN JV partner] has provided a counter guarantee to Arcadis, secured by a right of pledge of Logos Holding’s shares and voting rights in ALEN. Arcadis is able to exercise this right when Arcadis is requested to pay out under the guarantees provided to the lenders of ALEN and Logos Holding S.A. cannot pay Arcadis its share. This was however neither applicable nor expected as at 31 December 2018 as the lenders of ALEN did not make use of the guarantees received.

GUARANTEED BY EQUITY WORTH ZERO?

So whereas from a review of Arcadis’ 2017 financial statements one may have taken the view that the cross guarantees were cash backed, by the 2018 statements it is revealed that they are equity backed, where according to Arcadis the value of its ALEN equity is ZERO. On this basis, the guarantee against ALEN’s debt provided by the remaining 50.01% of equity in ALEN appears to us to be pointless.

It seems to us as rather obvious that the lenders of ALEN did not make use of the guarantees received. Primarily, as one of those primary lenders to ALEN is Arcadis itself. If Arcadis had made use of this, it may present difficulties in ALEN continuing to conduct business in Brazil and jeopardise any future sale of the business.

A GUARANTEE WITH P&L AND FUTURE CASH IMPLICATIONS?

In 2018, Arcadis reports that it impaired €31.8m of its shareholder loans to ALEN and provisioned for a further €22.1m in expected credit loss on shareholder loans and corporate guarantees to ALEN. This raises the following questions:

- Given that Arcadis has impaired and provisioned for a combined €53.9m on shareholder loans and corporate guarantees related to ALEN, is it only Arcadis that has borne the impact of this?

- Or has its JV partner also impaired and provisioned for losses on ALEN’s loans?

- If only Arcadis and not its JV partner, then why?

- Seeing as Arcadis has impaired its shareholder loans to ALEN, does this not demonstrate the folly of the apparent guarantees that Arcadis had provided on its own shareholder loans (see discussion above)?

- Why did Arcadis seemingly not make use of the cross guarantees it received against ALEN provided by the JV partner?

- While these guarantees appear to have no cash element to offset loans provided, Arcadis suggests that it could receive Logos Holding’s shares and voting rights in ALEN. Did it receive this?

- Why does Arcadis continue to extend new guarantees (€19m in 2019) to ALEN and its affiliates when, in our view, it doesn’t expect ALEN to be able to service its existing debt obligations?

- Why does Arcadis continue to report €87m in guarantees provided to ALEN, when according to its own 2018 financial statements, ALEN had €104.9m in loans (€49.8m) from external lenders and shareholder loans (€55.1m) from Arcadis? If €53.9m of this has been either impaired (€31.8m) or provisioned for (€22.1m) then we would have expected this to mean €51m was left to guarantee.

- Why does Arcadis appear to be the only lender to ALEN (out of the JV partners) that absorbs the impairment of its loans to ALEN, bears the risk of the remaining ALEN loans, and yet still only retains 49.99% interest?

€323M IN OTHER CORPORATE AND BANK GUARANTEES

With total corporate and bank guarantees of €409.5m in 2018, aside from the €87m attributable to ALEN, this leaves €322.5m related to other partners.

PROJECT PERFORMANCE RELATED OR AS DESCRIBED?

Within its 2018 financial statements, Arcadis describes these guarantees as follows (our bold for emphasis):

Arcadis has issued corporate guarantees as security for credit facilities and bank guarantee facilities. Bank guarantees are, amongst others, issued in relation to projects, advances received, tender bonds or lease commitments to avoid cash deposits. Bank guarantees issued for project performance can be claimed by clients where Arcadis fails to deliver in line with the agreed contract. In such cases, the liability of the bank should be no greater than the original liability on Arcadis and where the failure to perform arose due to an error or omission by Arcadis, the claim would be covered by the professional indemnity insurance cover.

However, on Arcadis’ Q4 2018 Earnings Call, its CEO, Mr Peter Oosterveer, seems to imply that these guarantees are largely related to small performance guarantees on projects with an average sum of just over €100,000 each (our bold for emphasis) [11]:

<Q – Philip Ngotho>: Philip Ngotho, ABN AMRO. My other question is I’m sure we will get more insights with the Annual Reports when it’s published, but can you give an indication of how the level of guarantees have developed this year versus last year? And my last question for now is on ALEN. I would like to know what’s your expectation is of the cash outflow for 2019. So, partly, I guess, the provision of €29 million, that would be a cash outflow, but what are the other expected cash outflows when looking at bringing the whole operations up and running. And also, why do you only project breakeven results in the second half of the year while the plans should be fully ramped up by then.

<A – Peter W. B. Oosterveer>: Okay. And so, maybe to help get a feel for the size of this, by the time you add it all up, it becomes a big number. But the reality is that it’s about – and don’t quote me on the exact numbers, 1,300 different guarantees which are performance guarantees on projects with an average of just over €100,000 each. So, if you had one big guarantee of €200 million versus [indiscernible] (00:54:00) €130,000 each, that’s a totally different picture. And that is the result of the type of business we conduct whereby a lot of clients, particularly in certain regions, are simply asking for performance guarantees on projects. But it is the sum of many small guarantees.

Our concern with the above description of events is that:

- It may be correct to suggest that Arcadis doesn’t have “one big guarantee of €200 million”, however, it does have one big guarantee of €87m related to ALEN, over which there is some doubt as to its recoverability.

- The big €87m guarantee with ALEN doesn’t appear to be project performance related and seems to be a straightforward guarantee of bank debt that ALEN has taken on. Further, as we have discussed above, there is seemingly no security over this guarantee other than equity which Arcadis has already valued at ZERO.

- The below table from Arcadis’ 2018 financial statements describes these guarantees as principally related to “debt facility” or “bank guarantee” financing, and that they reflect items that have been “drawn or utilized”. Therefore are they in reality much closer to the type of guarantees that relate to ALEN and less likely to be project performance related?

- If the guarantees are largely project performance related, then why do they now stand at 16.8% of net revenue, as compared to 5.9% in 2011? What does this say about the performance of Arcadis and its partners’ projects?

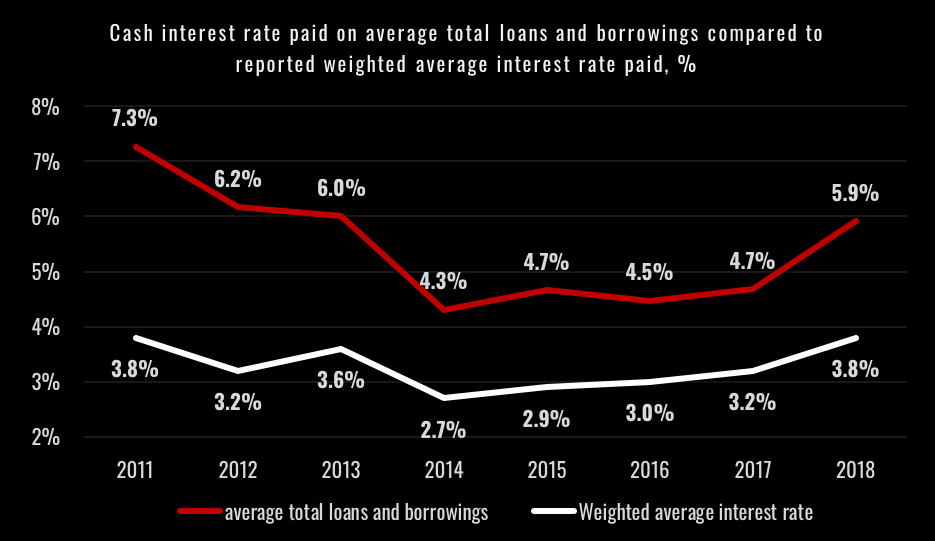

CASH OR INTEREST PAID IMPLIES A 5.9% RATE ON TOTAL LOANS AND BORROWINGS. WHY?

A feature of Arcadis’ financials that we are unable to reconcile is the level of cash interest the group pays as compared to its reported total loans and borrowings and weighted average interest rate.

Cash interest paid was €37.7m in 2018 (2017: €33.8m). Total loans and borrowings were reported to be €588.2m in 2018 (2017: €688.7m). Cash interest paid as a percentage of the average of the 2017 and 2018 loans balances works out to be 5.9% in 2018 (2017: 4.7%). However, Arcadis reports that its weighted average interest rate on interest-bearing debt (including the interest effect of swaps), was 3.8% in 2018 (2017: 3.2%).

We believe this differential makes little sense and if the reported weighted average interest rate of 3.8% is accurate, then the €37.7m in cash interest paid at this rate would imply average borrowings throughout 2018 of €992m [12].

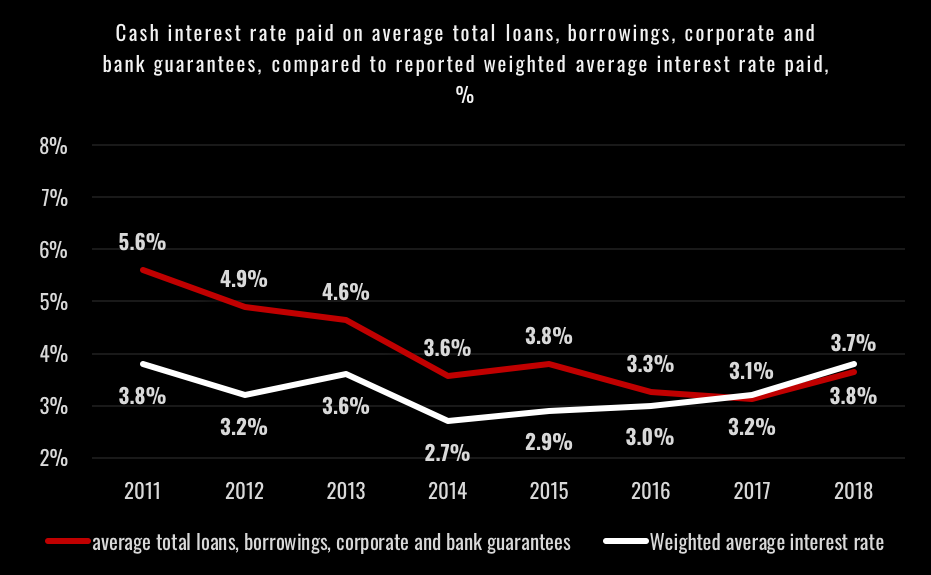

Another explanation may be that Arcadis is bearing the cost of servicing debt associated with the corporate and bank guarantees of its partners. Curiously, if Arcadis’ total loans and borrowings of €588.2m is combined with the €409.5m in corporate and bank guarantees is averaged for 2018, then its cash interest paid on this figure equates to 3.7%, i.e. remarkably close to its reported 3.8% weighted average interest rate.

In fact, if the weighted average interest rates which Arcadis reports each year are accurate, then for some time now its reported cash interest paid at this rate is typically close to what would be the interest rate paid on both Arcadis’ loans and borrowings and its corporate and bank guarantees. This can be seen in figure 8.

CAPITALISATION AND EBITDA

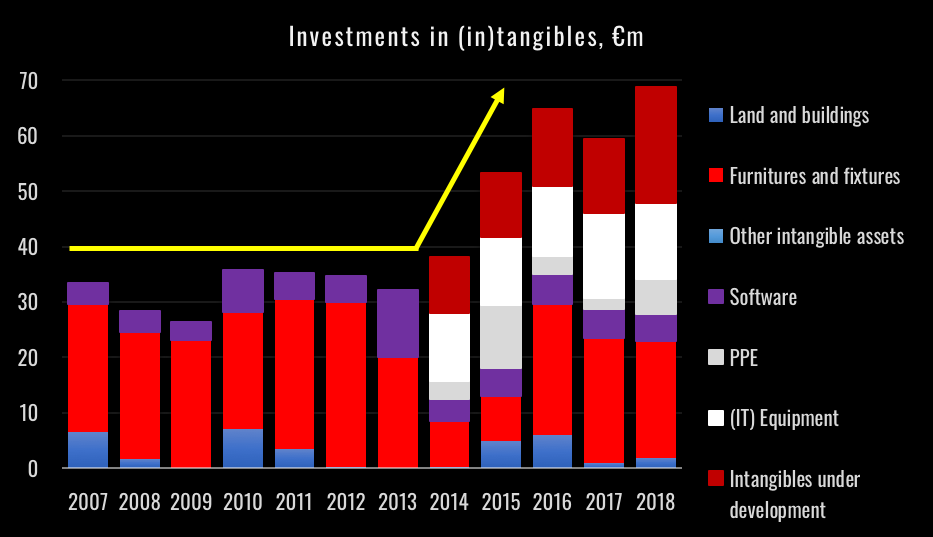

Whilst we see a growing stock of debt and liabilities off-balance sheet, we also see indications that Arcadis may be migrating increasing costs from its P&L to its balance sheet. Since 2013, Arcadis has more than doubled its expenditure on:

- Land and buildings;

- Furniture and fixtures;

- (IT) Equipment;

- Property, plant and equipment;

- Software; and

- Intangibles under development.

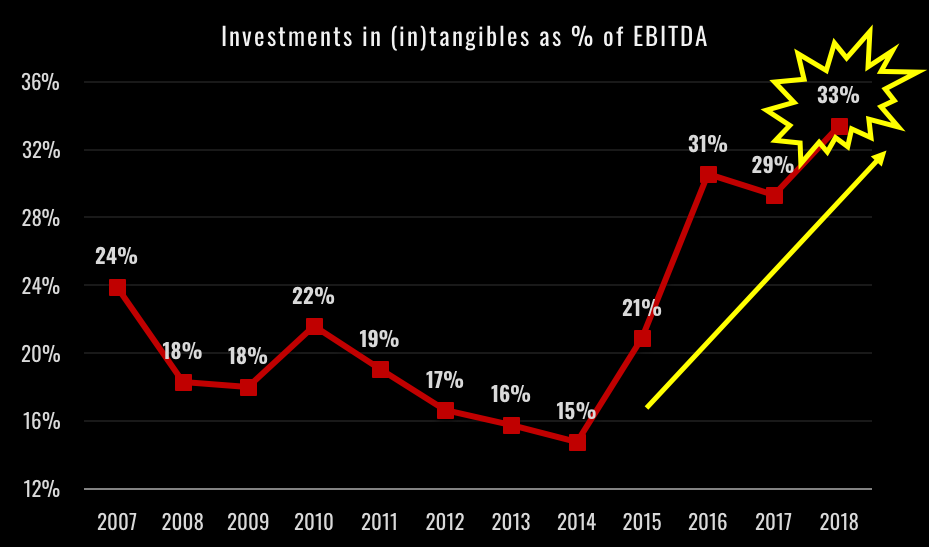

The principal driver of this increased expenditure has been intangibles under development (IUD). Whereas spending on IUD was reportedly ZERO in 2013, by 2018 it had risen to €20.9m, or 10.2% of 2018 EBITDA.

Overall, expenditure on the above items has risen from €32.2m in 2013, to €68.8m in 2018. In 2013, these items accounted for 15.8% of EBITDA. In 2018 these items accounted for 33.4% of EBITDA.

The costs associated with these items are capitalised, placed onto the Group’s balance sheet, and the related cash put through the investing section of Arcadis’ cash flow statement. In our experience, we see this as a classic indication of an effort to migrate costs from a company’s P&L to its balance sheet.

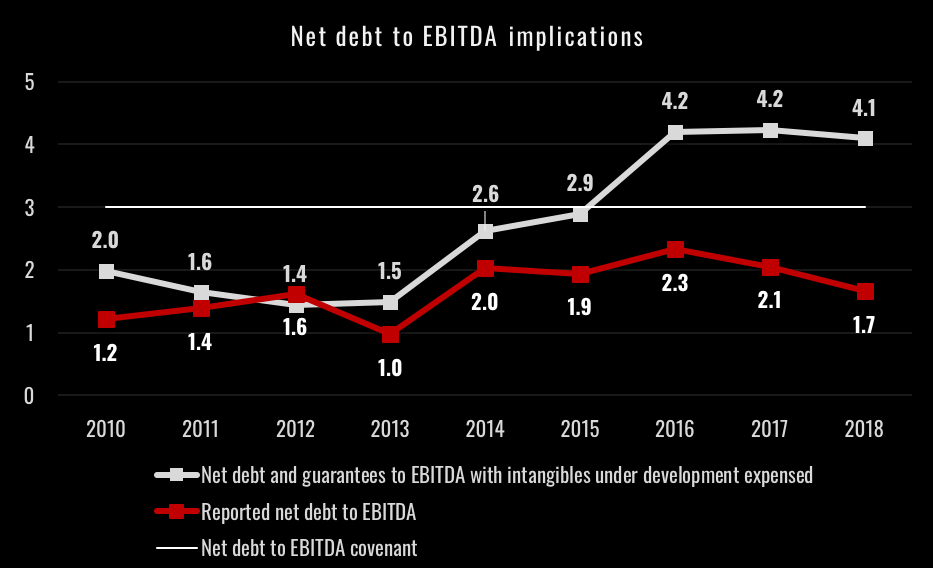

THE IMPLICATIONS OF ALL THIS…

Of course, if Arcadis’ guarantees of debt and bank guarantee facilities were brought onto its balance sheet, then its net debt may have been closer to €751.9m in 2018. Further, if Arcadis expensed the €20.9m in costs associated with intangibles under development, then its EBITDA would have been €184.9m in 2018. However, this might have implied that Arcadis was in breach of its debt covenant, with net debt to EBITDA ratio of 4.1x as compared to its reported 1.7x. This would be a wholly unsatisfactory thing to report. Or back to Latin, quod erat demonstrandum (Q.E.D.).

[1] Note: Mr Smith has written many interesting articles in the FT, we found this one particularly interesting as it touched upon phraseology we have seen utilised in the listed equity space.

[2] Ex ante: Adjective. Based on anticipated changes or activity in an economy.

Origin – Latin: Literally, from (what might lie) ahead; according to (what lies) ahead.

[3] Ex post: Adjective. Based on an analysis of past performance.

Origin – Latin: from (what lies) behind, according to (what lies) behind.

[4] Pro-forma: Adjective. In accounting, indicating hypothetical financial figures based on assumptions and projections (as opposed to actual past values).

Origin – Latin: from prō fōrma.

[5] Ultimo: Adverb. In or of the month preceding the current one.

Origin – Latin: Ultimō (mēnse or diē) in the last (month) or on the last (day).

[6] Arcadis 2018 financial statements – page 86: Covenants in loan agreements with banks stipulate that the average net debt to EBITDA ratio should be below 3.0, which is measured twice a year: at the end of June and at year-end. The calculation is based on the average of net debt at the moment of measurement and on the previous moment of measurement, divided by the (pro-forma) EBITDA of the twelve months preceding. According to this definition, the average net debt to EBITDA ratio at year-end 2018 was 2.0 (2017: 2.3). Arcadis’ long-term goal is a net debt to EBITDA ratio between 1.0 and 2.0.

[7] Arcadis 2018 financial statements – page 269: Average net debt ultimo for the year/EBITDA. A measure of a Company’s ability to pay off its incurred debt. This ratio gives the investor the approximate amount of time that would be needed to pay off all debt, excluding interest, taxes, depreciation and amortization.

[8] Arcadis 2018 financial statements.

[9] There is limited disclosure on this. Arcadis’ 2018 financial statements state: “The new guarantees [€19m] in 2019 relate primarily to new loans for the investments in the plant of one of ALEN’s affiliates and accrued interest.”

[10] Note that the ALEN affiliates received €16m in loans in 2017, which is also a material amount, and yet we were unable to find this disclosed in Arcadis’ 2017 financial statements.

[11] Arcadis Q4 2018 Earnings call. Source: Bloomberg

[12] Calculated as €37.7m divided by the reported 3.8% weighted average interest rate leads to average borrowings of €992m. This is some €404m higher than Arcadis’ reported total loans and borrowings at year end 2018.