Please read our Social Media Disclaimer when reading our ShadowFall Reflections.

THE EXPECTATION GAP

The recent, heightened interest in the role and responsibilities of audit firms and their oversight must raise conflicting views for short sellers. On the one hand, we at ShadowFall often rely on the market’s broad credulity regarding the significance of an audit. This general belief is that simply because a company’s set of financial statements is in receipt of a clean audit opinion, those statements are accurate and so may be relied upon. However, all an audit can provide is reasonable assurance by the auditor that the financial statements are accurate and free from misstatement whether due to fraud or error. In the Competition and Markets Authority’s Report, which we refer to further below, this is mentioned as the “expectation gap”. The expectation gap is generally deemed to be the difference between what the general public readers of the financial statements believe auditors are responsible for and what auditors themselves believe their responsibilities are.

SOME SYMPATHY? …

In our experience, a significant number of market participants fail to understand the basic function of what an audit provides. We believe that short sellers understand this function better, especially the fact that an auditor is not there to identify fraud, but to reasonably assure that fraud has not occurred. As testament to this, one should consider if they could name a mid-to-large scale corporate failure or fraud, which hasn’t been on the receiving end of a clean audit, i.e. corporate failures or frauds are rarely if ever highlighted by the audit.

In some cases there exists significant and sizeable collusive behaviour behind a fraud, and in this instance one might find it unreasonable to expect this to be discovered through normal statutory audit procedures. However, where less sympathy might reside is in regard to what is often referred to as aggressive accounting or accounting concerns. Especially when these concerns are raised by reputable, experienced individuals or firms within the public domain.

… BUT IF EVIDENCE OF A LACK OF PROFESSIONAL SCEPTICISM

Aggressive accounting is entirely legal and permissible. After all, “aggressive” is a subjective term. Were it not permissible then a company would fail its audit and audit failure is an altogether unsatisfactory event for a company hoping to remain a going concern. Our issue with aggressive accounting is that it is often a precursor either to corporate failure or a strong indicator of fraud. Further, that it is quite often identifiable in advance.

We believe regulators should be generally unsympathetic to auditors if ex-ante to financial distress or fraud the presence of aggressive accounting has been highlighted. If it’s possible for a reader of an Issuer’s accounts to recognize aggressive accounting, then it must be easier for the auditor to distinguish this when that auditor has access to the underlying material supporting those financial statements? This would be classed as a lack of appropriate professional scepticism on behalf of the auditor. In our experience, lack of professional scepticism appears particularly prevalent to audit reviews and judgements in regards to acquisitions, cost capitalisation, the valuation and impairment of assets, goodwill and other intangible assets, and the difference between average and year-end debt balances.

This seemingly habitual inability of an auditor to exercise appropriate professional define is undoubtedly the principal reason that most short sellers do not believe that audits are worth the paper they’re written on. In some instances a short seller may even be positively encouraged to see certain auditors as present in the accounts; especially particular regional offices of the Big Four.

CONFLICTS OF INTEREST

In the light of the increased focus on the audit market (see reports mentioned below) the conflicts of interest between an audit firm and its clients are again receiving greater scrutiny. But conflicts of interest are present among both short sellers and auditors. For our part, as short sellers we have a profit motive in electing to sell short an Issuer’s securities. The ShadowFall Fund is a short focused fund and so shorting is the principal manner in which returns are made for its investors. As such it is in the Fund’s interests to maintain the status quo of a credulous market and the aforementioned expectation gap. We prefer to identify the presence of aggressive accounting ex-ante financial distress by an Issuer, and certainly ahead of the Issuer’s auditor highlighting such concerns whether through outright audit failure or a qualified opinion.

Despite the profit motive of a short sale, at ShadowFall the initial draw to take such a stance is our view that the wider market is being deceived into thinking that an Issuer’s securities are worth more than our view of its intrinsic value. Without this fundamental belief there would be no serious prospect of profit. Profit is a potential corollary of hours of painstaking research.

Value deception is often driven by the manipulative, misleading or specious statements by such an Issuer’s management, that can result in financial loss or, in some instances, more pernicious outcomes. This irks us at ShadowFall, as we suspect it does most other prominent short sellers.

Across the market, among investors, sell-side analysts, and certain parts of financial media, the combination of the expectation gap and a clean audit can provide significant support when an Issuer’s management is unscrupulous. So the frequency with which audit firms not only evade culpability but even receive remuneration for failure to exercise appropriate professional scepticism in the audit process, is an ethically and morally bitter pill to swallow. This is especially so for any short seller whom aspires for greater scrutiny where it appears that financial or ethical rectitude by an Issuer may be missing.

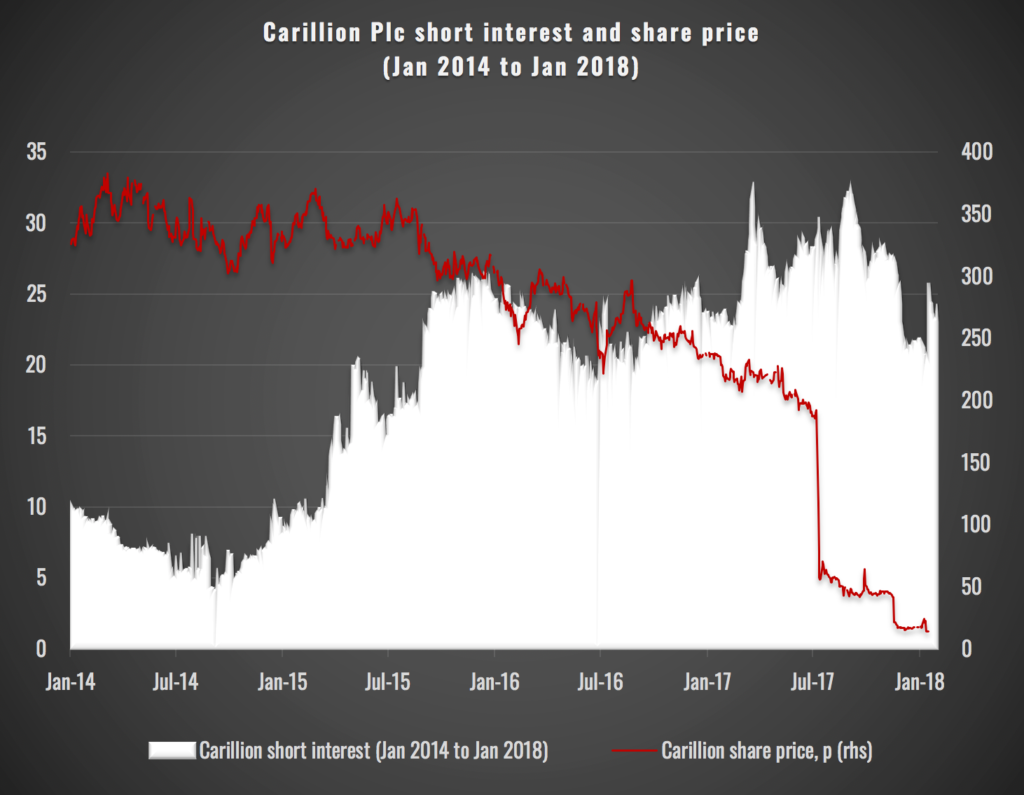

Figure 1 Carillion plc share price and short interest

Source: Bloomberg Finance L.P., IHS Markit

NO SURPRISES?

What is further exasperating is when accounting concerns are raised into the wider public domain. If both the auditor and any relevant oversight party is explicitly made aware of accounting issues, which are believed to exist, this notification still seems to too often fall on deaf ears. For example, Carillion plc is now widely held out as the poster child for an audit and oversight failure. As can be seen in the figure above, it was by no means a surprise to financial markets that Carillion’s equity was worthless. For at least three years prior to Carillion’s collapse into compulsory liquidation in January 2018, Carillion’s short interest was over 15% of its float. It even maxed out at 32.5% short interest in March 2017, a full 9 months prior to its failure. It is atypical for market participants to be willing to bet almost a third of a company’s share capital on the premise that its value is worth less than its prevailing value. In Carillion’s case, this should have set alarm bells ringing among its investor base, creditors, sell-side analysts, financial media and indeed its auditor, that there was a widely held belief that serious issues existed within Carillion. Indeed, these concerns were highlighted by the financial press well in advance of its ultimate collapse.[1] However, for Carillion’s audit firm, KPMG and the UK’s audit oversight body, the Financial Reporting Council (FRC), Carillion’s demise appears to have been something of a surprise.

INCREASING FOCUS ON THE UK’S AUDIT MARKET

In the UK, consternation regarding the failure of audit firms and oversight to foresee the financial distress that may fall upon their clients seems to be gaining ground. For example, in the Independent Review of the Financial Reporting Council (FRC), led by Sir John Kingman, the report states:

Part of the genesis of this Review was a concern in some quarters that a more effective FRC could do more to avert major corporate collapses, such as that of Carillion plc.[2]

The report goes on to describe the FRC as “a rather ramshackle house, cobbled together with all sorts of extensions over time.” This appeared to be a tacit belief by the report’s authors that the FRC was simply not fit for purpose and indeed the FRC is now in the process of being abolished.

The UK’s Competition and Markets Authority (CMA) highlights its own concerns within its recently published (18 December 2018) report, Statutory Audit Services Market Study. Among other aspects, the CMA report highlights the conflicts of interest which exist within audit firms, in terms of departments performing statutory audit work and those that provide more lucrative ancillary non-audit services. It is also not lost on the CMA that companies select and pay their own auditors, and that the selection of choice is relatively limited for the biggest firms, both factors which may impede the availability of sufficiently challenging and high-quality audits.

SHADOWFALL’S CONCERNS

The CMA report highlights a number of high-profile examples of audit failures within the UK, comprising both findings and open enforcement cases. The partners of ShadowFall have a strong record of highlighting accounting concerns. For example, of the current 26 concluded and open cases listed by the FRC, ShadowFall’s partners have raised accounting concerns for two of the concluded cases and another two of the open cases. Further, each time this has been well in advance of the FRC’s investigations.

RISK EQUILIBRIUM

As the ShadowFall Fund’s investors are aware, corporate governance and accounting concerns feature prominently within the theses on the Issuers we elect to short. That said, if our thesis is incorrect and we have made an error, then the Fund suffers and it and ShadowFall’s partners lose money. But we and our investors understand this risk and the scope of these losses is limited there. If an auditor signs off – what some may perceive as aggressively accounted – financial statements for an Issuer, then if the Issuer is subsequently determined to be a fraud, the consequences are much greater. So how do auditors suffer in this event? In our view too frequently too lightly.

Oliver Shah, Business Editor of the Sunday Times, highlighted this a few weeks ago in an article: Blunt instruments won’t solve audit puzzle. Mr Shah suggests:

“The quickest way to improve audit quality would be to make the partners of accountancy firms concentrate on a smaller number of clients and to explore ways of holding them – and the audit committees who appoint them – responsible when things go wrong.”

We believe this forms the correct approach to take. Few factors sharpen the mind’s focus more than risk of incurring significant financial losses. If auditors faced this risk then their interests would be better aligned with shareholders. This can can only be a good thing.

[1] Financial Times: Anatomy of a trade – the persistence of Carillion’s short sellers (6 April 2017)

[2] Independent Review of the Financial Reporting Council – page 14. For reference, Carillion Plc was a UK listed (CLLN LN) Construction and Services firm, which filed for compulsory liquidation in January 2018.