TESTING TIMES…UNLESS YOU’RE A TESTER

Unlike some of the Covid-19 vaccine manufacturers, when it comes to testing for Covid, many believe that extortionate profits are being made by the providers of PCR tests. However, few seem able to determine just how much profit is being made. In our analysis below, we find that sensible assumptions point towards 50%+ profit margins being achieved by some PCR test providers. Given that these tests have been a mandated requirement to carry on with a normal life, we question whether it is socially acceptable that such significant profiteering is taking place.

“The performance predominantly reflected the significant impact of the equitable supply, at no profit to AstraZeneca, of the pandemic COVID-19 vaccine . . . .”

AstraZeneca 1H21 results

Much has been written over recent weeks in the UK press regarding what is widely viewed as extortionate pricing of PCR tests. As Sky News reported on Monday, 9 August 2021:

‘The Health Secretary [Sajid Javid MP] has asked the competition watchdog to investigate the market for PCR tests amid concerns of “exploitative practices” and vastly different costs.’

In the UK, on 14 August 2021, the Government announced the:

“List of private testing providers to be reviewed to ensure pricing is accurate and transparent.”

Then on Sunday 22 August 2021, the Sunday Times highlighted the EUR 1 billion boost to sales of one particular testing provider, Eurofins:

“The figures come amid growing anger over perceived overcharging by companies for Covid testing. Eurofins’ share price on the Paris stock exchange has almost doubled in the past year, leaving founder Gilles Martin’s family stake surging above €3 billion.”

While many are rightly angry about the absurd costs of these tests and have a strong sense that some form of profiteering is likely taking place, seemingly few can work out just how much profit is being made.

We believe that we might be able to provide some insight.

EUROFINS SCIENTIFIC SE

Eurofins is a EUR 22.8bn market value, French listed provider of analytical testing services to the pharmaceutical, food, environmental, and consumer products industries.

ShadowFall holds a short position in Eurofins.

Eurofins is a company that we have been familiar with for some time. Indeed, we shared some of the issues we had identified in October 2019, which included:

- What we perceived as strange lending of millions of euros to a Panamanian owned entity.

- The elaborate nature of Eurofins’ corporate structure.

- Inconsistencies we discovered regarding profitability and net asset values among its subsidiaries.

- Discrepancies we found between related party transactions.

- Many cases of either multiple owners of the same subsidiary or seemingly absent owners.

Since then, the group has experienced what we believe to be a profit boon from providing significant testing services for Covid-19.

THE MARGIN BOOST

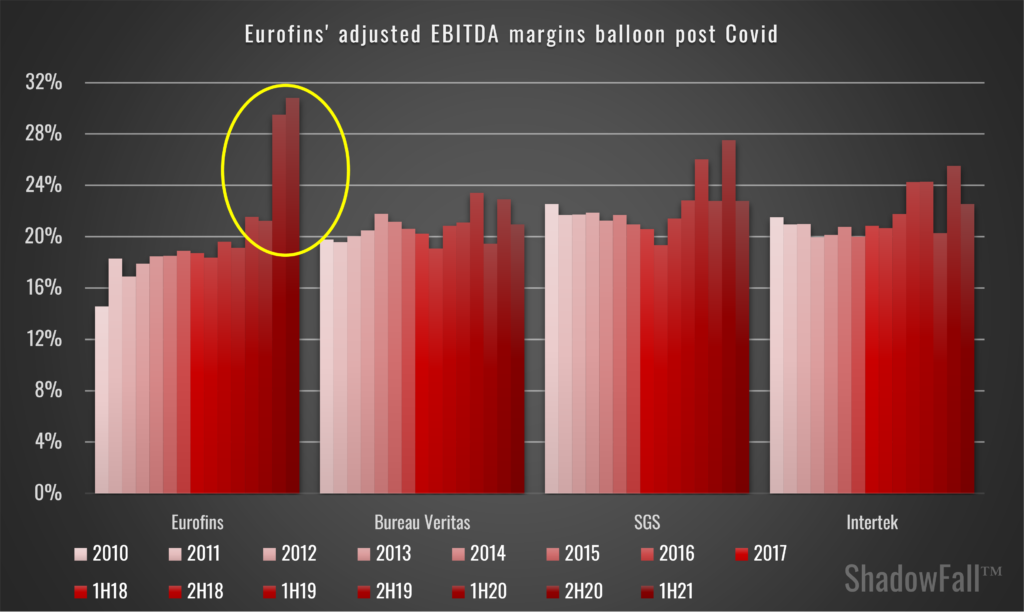

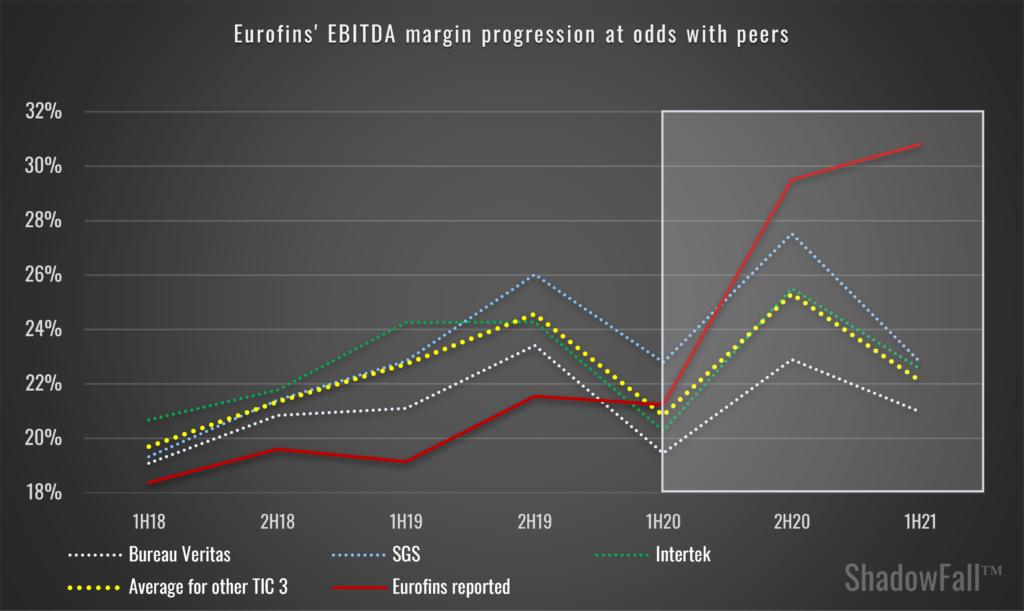

Figure 5 shows the adjusted EBITDA margins for Eurofins, Bureau Veritas, SGS and Intertek; four of the largest, listed providers in the Testing, Inspection & Certification (TIC) market. The data goes back to 2010, although since 2018 the margins are detailed on a half yearly basis. Does anything catch your eye?

From a margin perspective, the Covid period has been good for the TIC market. Although in Eurofins’ case … it’s been really good!

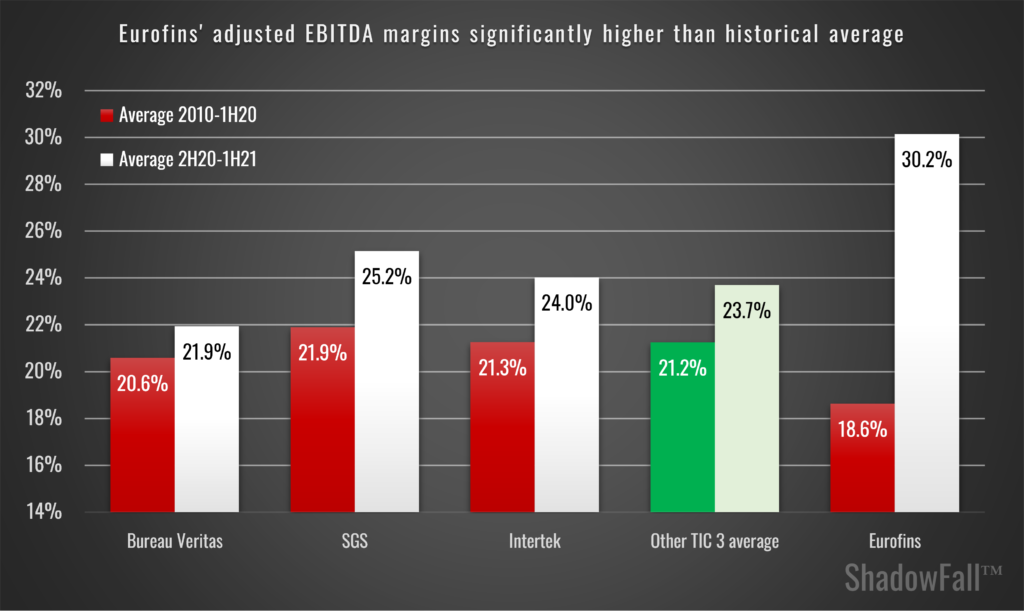

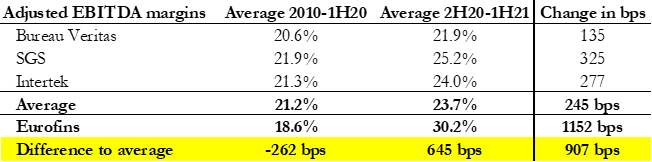

Compared to Eurofins’ average EBITDA margin during the period 2010 to 1H20, Eurofins’ EBITDA margin in the period 2H20 to 1H21 has risen a remarkable 1,152 bps. Further, comparing this to the other three TIC companies demonstrates just how significant the boost to Eurofins’ profitability there has been during the Covid period. Eurofins’ 1,152 bps margin improvement is a remarkable 4.7x of the average 245 bps rise which the other three TIC companies have experienced during the same period (figure 7).

THE DIFFERENCE: COVID TESTING?

When it comes to Covid testing related business, Eurofins handily provides guidance regarding how much of its revenue relates to Covid testing. Less helpful is that it doesn’t offer insight into how much profit it is making on its Covid related revenue.

For example, from its 1H21 results, Eurofins stated (our bold for emphasis):

“Strong growth of revenues, resulting in a record six-month period with EUR 3,272m revenues in H1 2021 up 41% vs. H1 2020, thanks to strong growth of Eurofins’ Core Business (excluding COVID-19 related clinical testing and reagent revenues) and sustained revenues from COVID-19 testing and reagents (close to EUR 750m).”

AND PROFIT?

One way to gauge how much Covid related profit Eurofins might be making is by simply looking at how its peers have performed which haven’t had any Covid related profit. Then we can strip out an implied Covid related EBITDA margin. If we do this, then the results show that Covid related profit is extremely high.

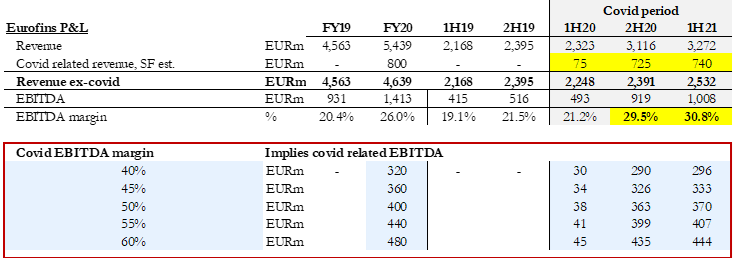

Based on company disclosure and management comments, we estimate that Eurofins had a Covid revenue contribution of EUR 75m, EUR 725m and EUR 740m in 1H20 to 1H21 respectively. This contribution has been material and compares to Eurofins’ core revenue (ex-Covid related) as shown in figure 8.

As mentioned above and shown in figure 9, Eurofins’ EBITDA margin has dramatically risen during the Covid period.

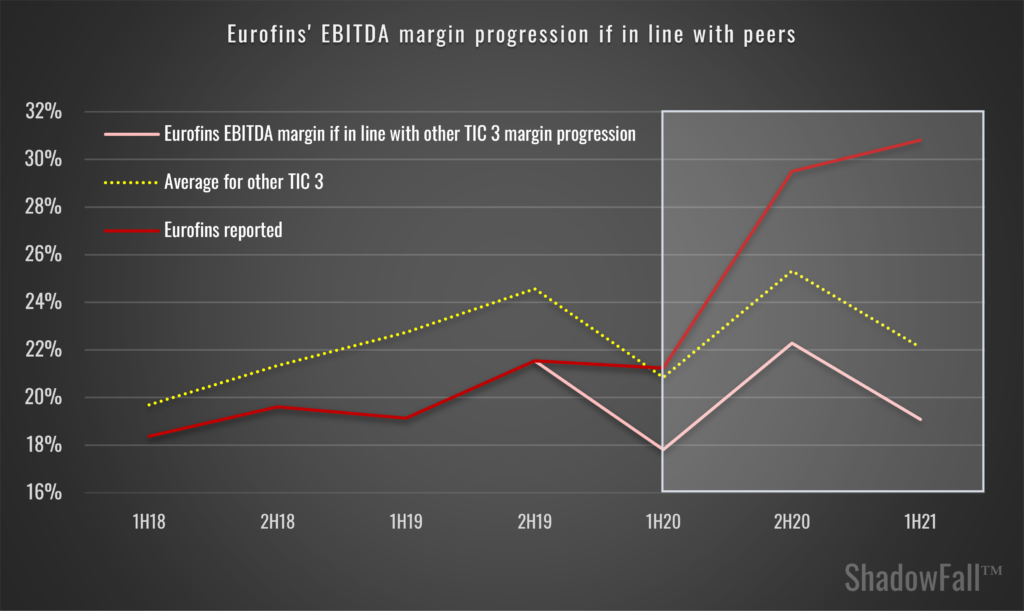

But again, we are drawn to the fact that EBITDA margin progression among the other TIC providers – which haven’t had a Covid boost – has been less spectacular (figure 10).

We believe that this all sort of begs the question, what if Eurofins’ EBITDA margins had progressed in line with the average trend experienced by the other TIC 3 providers. This is shown in figure 11.

Under the scenario seen in figure 11, the significant margin progression – which Eurofins has enjoyed (figure 7) – would have principally stemmed from Covid-related revenue. Of course, if the core margin (ex-Covid) had developed in line with peers to 19.1% in 1H21, then this would imply that the EBITDA margin on Covid related revenue would have been 71% in 1H21. That to us seems remarkably high.

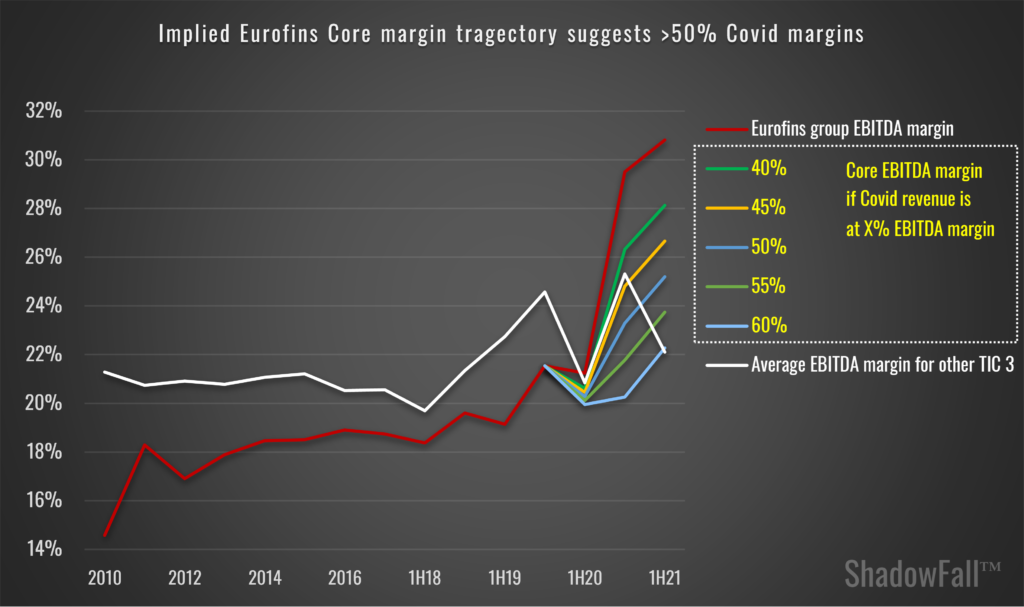

SO, WHAT IF COVID RELATED EBITDA MARGINS WERE AS HIGH AS 50%?

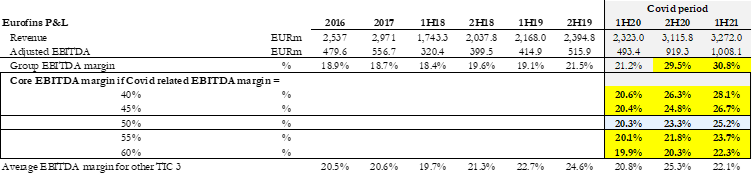

In figures 12 and 13, we analyse several scenarios regarding the implications for EBITDA margins within Eurofins’ core business if Covid related EBITDA margins were to range between 40% and 60%.

Our scenario analysis shows that when Covid-related EBITDA margins reach 50%, the implied core business adjusted EBITDA margin rises by 366bps, to 25.2% in 1H21 (from 21.5% in 2H19) (see figure 12). This is still an astonishing increase in the core margin and certainly in the context of the company’s historical EBITDA margins which averaged 19.7% during the two years prior to the Covid pandemic. Starker still, this would compare to a performance among the other TIC 3 providers, where margins rose on average by 245bps during the same period (see figure 7).

We believe that this simple analysis of EBITDA margin scenarios demonstrates just how material Covid might have been for Eurofins. For example, as figure 14 shows, if the EBITDA margin on Covid related revenue is 50%, then in 1H21, this would suggest that Covid related EBITDA equated to EUR 370m, or 36.7% of the total group adjusted EBITDA of EUR 1,008m in 1H21.

ARE 50%+ MARGINS ACCEPTABLE?

If any of the above scenarios are an accurate reflection of matters, we question the social benefit of companies which achieve such significant profit margins at either a cost to taxpayers, private individuals or both. Especially, when those having to pay for the tests are essentially forced to take them to continue with some semblance of a normal life. Holiday goers are frequently quoted as having felt a dent in their wallets when being required to take compulsory PCR tests to travel abroad.

Aside from the social cost, the above scenarios raise another issue which Eurofins’ investors may wish to keep an eye on ….

TOO MUCH CASH!

In March 2019, on the FY18 results call, Eurofins’ CEO, Dr Gilles Martin, lamented (our bold for emphasis):

“We had too much cash at the end of last year, I found out. I was not very pleased with our treasurer actually because we had about €500 million –we shouldn’t have ended the year with €500 million cash.”

By May 2020, it seems to us that there wasn’t enough cash. Eurofins announced an accelerated book build, raising EUR 535 million, stating (our bold for emphasis):

“The purpose of this Placement is to enable Eurofins to fund investments and net working capital needs in conjunction with the build-up of its capacity in COVID-19 related PCR tests, serologic tests and internal manufacturing of kits, probes and primers as disclosed in its Q1 2020 results publication made on 28 April 2020 . . . .

. . . . This issuance would also enable Eurofins to further strengthen its current capital structure to be an even stronger company when the COVID-19 crisis will end and to have more strategic flexibility to seize potential investment opportunities then, with an objective to generate long term shareholder value and create a higher EPS than the dilution impact of the new issuance. Further to the successful equity issuance of October 2017, this Placement will give qualified institutional investors an opportunity to participate in the offering and in Eurofins’ future development, while increasing further the liquidity in Eurofins’ shares.”

TOO MUCH COVID CASH!

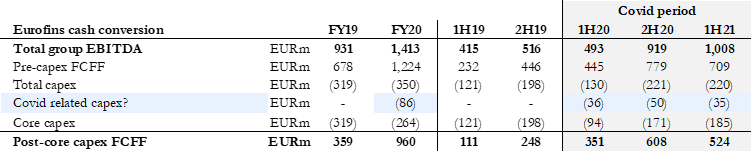

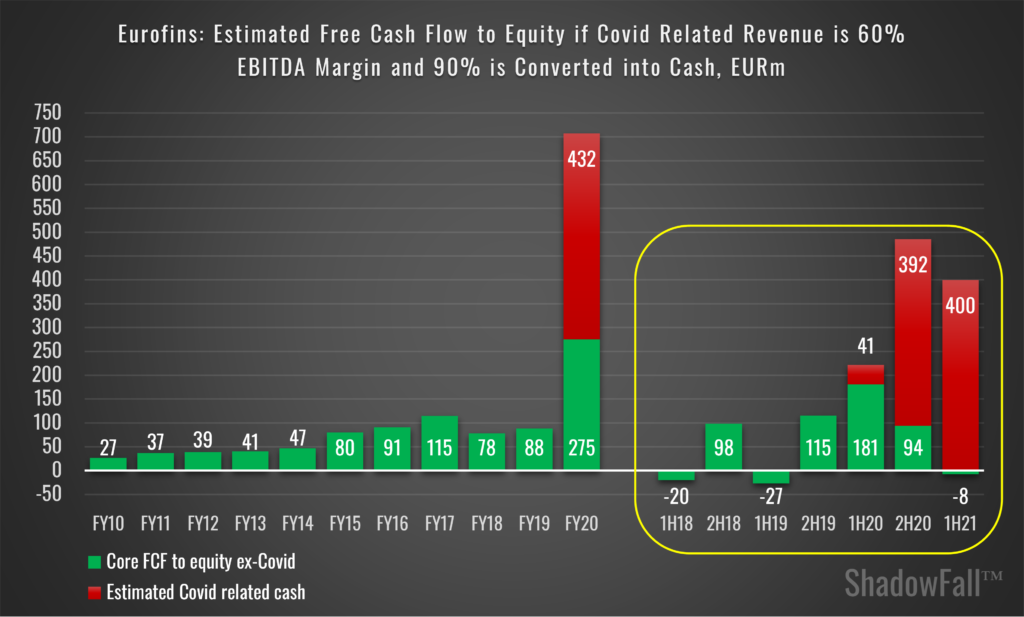

With such material Covid related profit, our next question is how much of this is converted into cash? To answer this, we have performed a sensitivity test looking at Covid-related EBITDA and conversion of this into cash which can be seen in figure 15. According to this scenario analysis, if 1H21 Covid-related revenue of EUR 740 million achieved a 50% EBITDA margin, equating to EUR 370 million in EBITDA, and 90% of this was converted into cash, then Eurofins hauled in EUR 333 million of Covid related cash in 1H21 and EUR 659.3 million on a trailing twelve-month (TTM) basis. In our view, cash conversion is likely to be extremely high for Covid testing and could be even greater than 90%.

EUR 333 million is a fair chunk of cash. In fact, it would have equated to 47% of Eurofins’ EUR 709 million in total pre-capex Free Cash Flow to the Firm (FCFF) in 1H21. So, despite Covid related revenue accounting for c. 22.6% of total group revenue in 1H21, cash wise it may have accounted for nearly half of the group’s cash generation.

Our view is that the implications are possibly worse than this.

WHAT IS THE CAPEX REQUIREMENT RELATED TO THE COVID TESTING?

Eurofins has alluded to this. For example, in its 2020 annual report, the group stated that net capex was EUR 350m, which was above the EUR 300m guidance the company set in March 2020. Eurofins indicates that c. 35% of this, EUR 122.5m, reflected both lab equipment capex related to Covid-19 testing and the completion stages of its infrastructure programme (our bold for emphasis):

“Net capex spend increased by 9.7% year-on-year to EUR 350m in FY 2020 compared to EUR 319m in FY 2019 and represented 6.4% of Group’s revenues vs. 7.0% in FY 2019, slightly above the Group’s initial objective of EUR 300m set in March 2020 and reflecting the initial Net capex freeze implemented at the start of the COVID-19 pandemic, which was subsequently offset by the requirements to ramp up the Group’s COVID-19 testing capacity. Laboratory equipment represented ca. 35% of the total FY 2020 Net capex spend, reflecting both the ramp-up in our COVID-19 testing capacity and the completion stages of our infrastructure programme. Buildings and leasehold improvements represented ca. 40%, consistent with the finalisation of our hub and spoke network following the significant acquisitions made in 2017 and 2018, and IT spend amounted to ca. 20%, in line with our sustained effort to develop unique laboratory information management systems (LIMS) and accompany the digital transformation of our activities.”

At a maximum, it appears that Covid related lab equipment capex equated to EUR 122.5 million in FY20 (c. 35% total capex of EUR 350 million). Further, in the past 18 months to 1H21, Eurofins has reported a EUR 176 million cash drag relating to working capital. If we assume that all the EUR 122.5 million in capex related to Covid lab equipment and all this working capital related to Covid testing roll-out, then this equates to EUR 298.5 million. And yet, the group raised EUR 535 million in April 2020, leaving EUR 236.5 million left over. Again, too much cash!

The reality, however, is that this is as generous as one could be towards Eurofins. The likelihood is that a significant portion of the capex was to do with the as mentioned “completion stages of our infrastructure programme”. Further, any working capital outflow was likely largely to do with core business, which Eurofins’ reports to have grown very strongly in the recent period. After all, Eurofins has always consumed working capital as its core business has grown in the past.

In fact, since private customers must pay ahead of receiving the PCR test, one would presume that this results in materially better days sales outstanding (DSOs) than the existing core business. Further, any government related Covid revenue is likely also on good payment terms. Therefore, our view is that as well as ultimate profitability, Covid has also been beneficial from a working capital perspective.

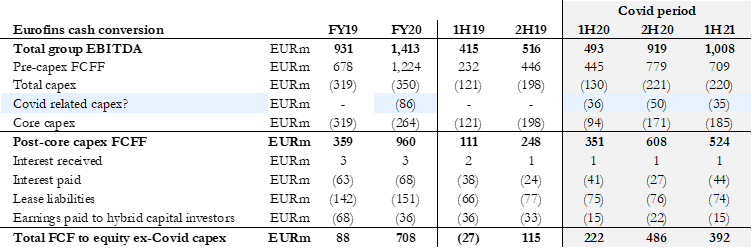

We estimate that Covid-related capex was EUR 36m in 1H20, EUR 50m in 2H20 (c. 70% of the EUR 122.5m split between Covid related and completion of the infrastructure programme), and a further EUR 35m in 1H21. Using these inputs would mean (as shown in figure 16) that Eurofins generated EUR 524 million in post-core (ex-Covid related) capex Free Cash Flow to the Firm (FCFF) in 1H21.

However, to arrive at Free Cash Flow to Equity (FCFE) there are net interest, lease liabilities and earnings paid to hybrid capital investors. These cash costs are likely required regardless of Covid or not. Accounting for these we arrive at EUR 392 million in FCFE in 1H21 (as shown in figure 17).

But then if 1H21 delivered:

- EUR 740 million in Covid related revenue.

- EUR 370 million in Covid related EBITDA (50% margin); and

- EUR 333 million in Covid related cash (EBITDA converted at 90%).

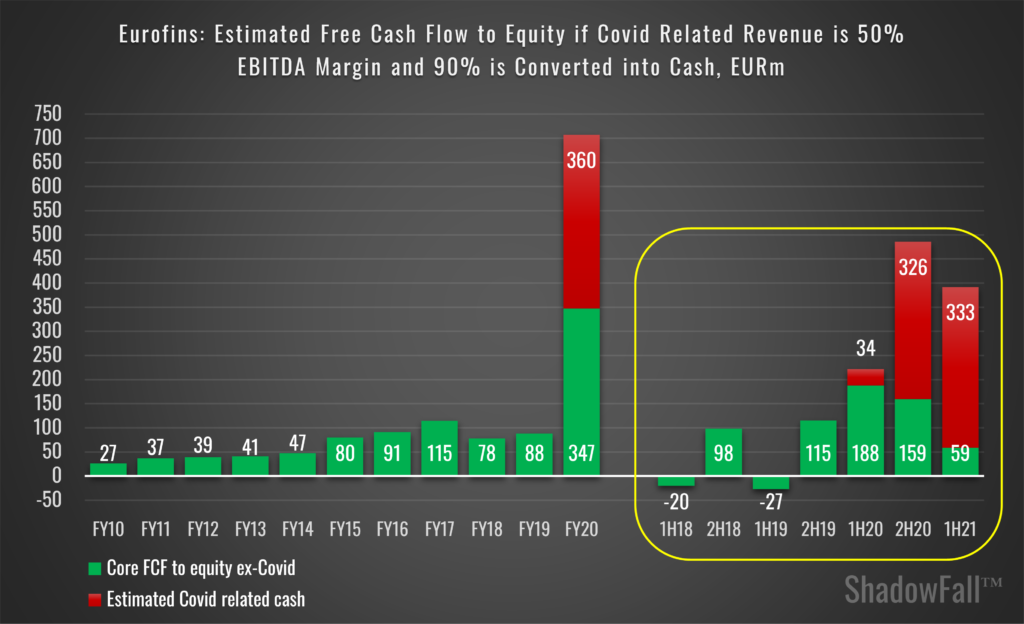

Then without the Covid related cash contribution in 1H21, FCFE would have been EUR 59 million (see figure 18). Given that this is on the back of a self-described “record performance” in 1H21, we would argue that this is not particularly attractive. Then again, weak cash generation to equity compared to ever growing profitability is something that we believe Eurofins has demonstrated for eons (see figure 19).

If Covid related revenue is at a 60% EBITDA margin, then the cash implications for the Core business appear to us to be far worse still (figure 19).

SO, WHAT IS ALL THIS COVID TESTING WORTH? THE MARKET THINKS 7-10x!

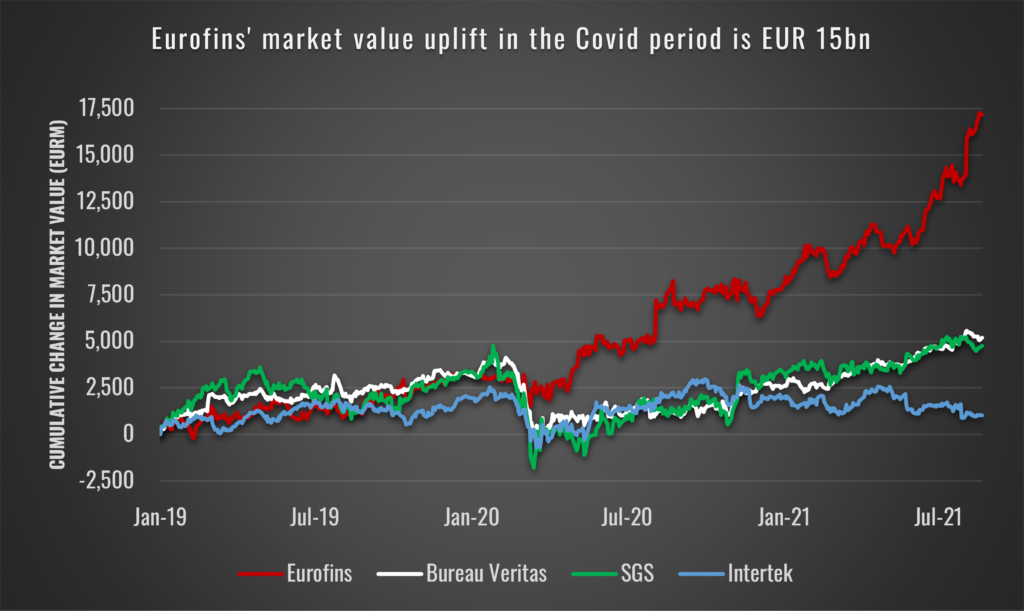

Eurofins’ shareholders have been generously rewarded for having a position since the start of the Covid pandemic. Since year end 2019, Eurofins stock has rallied from EUR 49.4 to EUR 118.5; a return of 140%. Undoubtedly, a contributing factor to the plentiful return shareholders have received has been the significant Covid testing contribution to EBITDA we have discussed above.

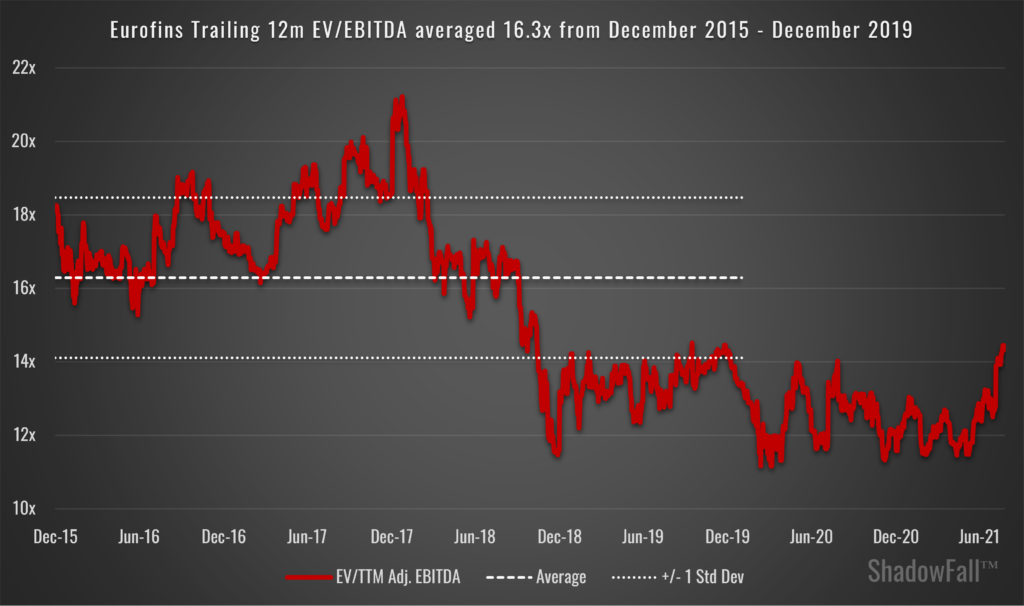

Prior to Covid, Eurofins traded on what we calculate to be an average of 16.3x trailing twelve-month EV to Adjusted EBITDA, during the period December 2015 – December 2019 (see figure 20). We exclude the initial 1Q20 period from our calculation due to the market wide sell off.

To estimate the value therefore which the market is applying to these Covid revenues, we assume that the Core business EBITDA is valued at this same 16.3x trailing twelve month (TTM) Adjusted EBITDA.

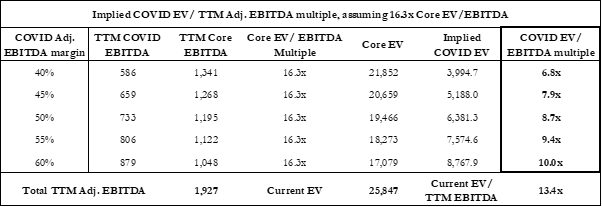

If we look at the scenario where Covid EBITDA margins are at 50%, this implies Core TTM EBITDA of EUR 1,195 million. Valuing this Core EBITDA at 16.3x provides an EV estimate of EUR 19.5 billion for Eurofins, compared to the current EV of EUR 25.8 billion.

Therefore, the implied value being associated to the Covid testing business is a significant EUR 6.4 billion, which we calculate to be a trailing 8.7x EBITDA multiple. Significant, we would argue, for what we all hope is a limited-lifetime revenue stream.

If Covid testing revenues achieve the higher 60% margin – which given our analysis above, we don’t believe is particularly unrealistic – then, we calculate that TTM Core EBITDA would be EUR 1,048 million. This corresponds to a value of EUR 17.1 billion. Therefore, Covid testing business is assigned an EV of EUR 8.8 billion or a 10.0x trailing EBITDA multiple. Punchy.

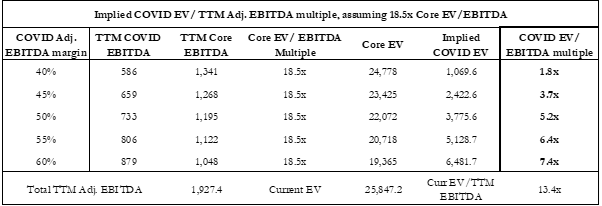

Some may argue that the core business has re-rated since the December 2015 – December 2019 period, due to the apparent improving momentum in the core business. Figure 22 below completes the same analysis however valuing the Core EBITDA on a trailing 18.5x EBITDA multiple, 1 standard deviation above the December 2015 – December 2019 average.

Using the same 50-60% range in Covid testing EBITDA margins, we calculate that the market is assigning an EV to the Covid testing business of between EUR 3.8 billion and EUR 6.5 billion, or a 5.2x – 7.4x trailing multiple.

Of course, how much profit and cash is attributable to Covid, and what implied value is being attached to Covid related profit could all be far more easily determined if Eurofins were to detail exactly what profit margin and cash conversion it has achieved on these Covid revenues in the 18 months past. Perhaps the UK Health Secretary, Sajid Javid MP, may be able to get to the bottom of all this following the competition watchdog’s inquiry.

Published 3:30pm 25th August

Contact: [email protected]

Terms & Conditions:

ShadowFall Publications Limited’s terms and conditions (collectively, these “Terms”) are available here on the ShadowFall website (www.ShadowFall.com) and set out the basis on which you may make use of the ShadowFall website and its content, whether as a visitor to the ShadowFall website or a registered user. Please read these Terms carefully before you start to use the ShadowFall website.

By using, downloading from, or viewing material on the ShadowFall website you indicate that you accept these Terms and that you agree to abide by them. If you do not agree to these Terms, you must not use the ShadowFall website nor any of its content.

You must not communicate the contents of this website blog entry (“entry”) and other materials on this website to any other person unless that person has agreed to be bound by these Terms. If you access this website, download or receive the contents of website blog entries or other materials on this website as an agent for any other person, you are binding your principal to these same terms.

Disclaimer and Disclosures:

This entry, which contains an implicit recommendation, has been produced by ShadowFall Publications Limited which is an Appointed Representative (FRN 842414) of ShadowFall Capital & Research LLP which is authorised and regulated by the Financial Conduct Authority in the United Kingdom (FRN 782080) (together “ShadowFall”) and published onto the ShadowFall website (www.ShadowFall.com).

Any information which could be construed as investment research has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is also not subject to any prohibition on dealing ahead of the dissemination of investment research. Unless otherwise specified, the information and opinions presented or contained in this entry are provided as of the date of this entry. ShadowFall is under no obligation to update, revise or affirm this entry.

ShadowFall Capital & Research LLP manages and advises investment funds and managed accounts (the “funds”) which inter alia takes positions in traded securities. At the time of publication on the ShadowFall website on 25th August 2021 , the funds hold short positions in Eurofins Scientific, which may include through options, swaps or other derivatives relating to the issuers. The funds may take further positions in the issuers (long or short) at a future date. In addition, at the time of publication on the website, the Managing Partner of ShadowFall is invested in a funds managed by ShadowFall Capital & Research LLP.

Neither the authors nor ShadowFall are aware of any factor, subject to the paragraph above, which might reasonably be expected to impair their objectivity in the preparation of this entry. The authors and ShadowFall are not aware of any direct or indirect conflicts of interest, subject to the paragraph above, that might exist between the authors or ShadowFall and any issuer which is the subject of this entry (the “issuer”). In particular, neither the author nor ShadowFall has any affiliation with the issuer.

ShadowFall has taken all reasonable steps to ensure that factual information in this entry is true and accurate. However, where such factual information is derived from publicly available sources ShadowFall has relied on the accuracy of those sources.

Some of the open-source data contained in this entry may have been sourced from public records made available by Companies House, which is licensed under the Open Government License; https://www.nationalarchives.gov.uk/doc/open-government-licence/version/3/

All statements of opinion contained in the entry are based on ShadowFall’s own assessment based on information available to it. That information may not be complete or exhaustive. No representation is made, or warranty given as to the accuracy, completeness, achievability or reasonableness of such statements of opinion.

This entry is only intended for investors who qualify as FCA defined Professional Clients (the “Recipient(s)”), who are expected to make their own judgment as to any reliance that they place on the content of the entry. This entry is not suitable for, nor intended for any persons deemed to be a “Retail Client” under the FCA Rules. In addition, the content of this entry is not intended for any jurisdiction outside which ShadowFall is not authorised.

This entry is for informational purposes only and is not an offer or solicitation to buy or sell any investment product. This entry is the property of ShadowFall.

ShadowFall does not take responsibility or accept any liability for any action taken or not taken by the Recipients of this entry as a result of information and/or opinions contained in the entry. Specifically, Recipients of this entry agree to hold harmless ShadowFall and its affiliates and related parties, including, but not limited to any partners, principals, officers, directors, employees, members, clients, investors, consultants and agents (collectively, the “ShadowFall Related Persons”) for any direct or indirect losses (including trading losses) attributable to any information and content on the ShadowFall website including any publications on the website.

In no event shall ShadowFall or any ShadowFall Related Persons be liable for any claims, losses, costs or damages of any kind, including direct, indirect, punitive, exemplary, incidental, special or, consequential damages, arising out of or in any way connected with any information or content on the ShadowFall website or in this entry.

Recipients must exercise their own judgment and where appropriate take their own investment, tax and legal advice prior to taking or not taking action in reliance on the contents of this entry.

Forward-looking information or statements in this entry may contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. ShadowFall makes no representation herein that forward-looking predictions shall come to pass. ShadowFall is committed to providing services and products which are unbiased and impartial and have implemented a Conflicts of Interest Policy pursuant to FCA rules.