Published: 22 April 2020 – 15:20

Contact: [email protected]

Terms & Conditions:

ShadowFall Publications Limited’s terms and conditions (collectively, these “Terms”) are available here on the ShadowFall website (www.ShadowFall.com) and set out the basis on which you may make use of the ShadowFall website and its content, whether as a visitor to the ShadowFall website or a registered user. Please read these Terms carefully before you start to use the ShadowFall website.

By using, downloading from, or viewing material on the ShadowFall website you indicate that you accept these Terms and that you agree to abide by them. If you do not agree to these Terms, you must not use the ShadowFall website nor any of its content.

You must not communicate the contents of this website blog entry (“entry”) and other materials on this website to any other person unless that person has agreed to be bound by these Terms. If you access this website, download or receive the contents of website blog entries or other materials on this website as an agent for any other person, you are binding your principal to these same terms.

Disclaimer and Disclosures:

This entry, which contains an implicit recommendation, has been produced by ShadowFall Publications Limited which is an Appointed Representative (FRN 842414) of ShadowFall Capital & Research LLP which is authorised and regulated by the Financial Conduct Authority in the United Kingdom (FRN 782080) (together “ShadowFall”) and published onto the ShadowFall website (www.ShadowFall.com) on 22 April 2020. Extracts of this entry were first distributed to clients of ShadowFall on 3 March 2020 and further highlighted in a ShadowFall Investor Letter dated 14 April 2020.

Any information which could be construed as investment research has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is also not subject to any prohibition on dealing ahead of the dissemination of investment research. Unless otherwise specified, the information and opinions presented or contained in this entry are provided as of the date of this entry. ShadowFall is under no obligation to update, revise or affirm this entry.

ShadowFall Capital & Research LLP manages an alternative investment fund (the “fund”) which inter alia takes positions in traded securities. At the time of publication on the ShadowFall website on 22 April 2020, the fund holds a short position in the following issuers covered in this entry; St James Place plc, and the fund holds a long position in the following issuers covered in this entry; Aviva plc; which may include through options, swaps or other derivatives relating to the issuers. The fund may take further positions in the issuers (long or short) at a future date. In addition, at the time of publication on the website, an author of this entry is invested in the fund.

Neither the authors nor ShadowFall are aware of any factor, subject to the paragraph above, which might reasonably be expected to impair their objectivity in the preparation of this entry. The authors and ShadowFall are not aware of any direct or indirect conflicts of interest, subject to the paragraph above, that might exist between the authors or ShadowFall and any issuer which is the subject of this entry (the “issuers”). In particular, neither the author nor ShadowFall has any affiliation with the issuers.

ShadowFall has taken all reasonable steps to ensure that factual information in this entry is true and accurate. However, where such factual information is derived from publicly available sources ShadowFall has relied on the accuracy of those sources.

Some of the open-source data contained in this entry may have been sourced from public records made available by Companies House, which is licensed under the Open Government License; https://www.nationalarchives.gov.uk/doc/open-government-licence/version/3/

All statements of opinion contained in the entry are based on ShadowFall’s own assessment based on information available to it. That information may not be complete or exhaustive. No representation is made, or warranty given as to the accuracy, completeness, achievability or reasonableness of such statements of opinion.

This entry is only intended for investors who qualify as FCA defined Professional Clients (the “Recipient(s)”), who are expected to make their own judgment as to any reliance that they place on the content of the entry. This entry is not suitable for, nor intended for any persons deemed to be a “Retail Client” under the FCA Rules. In addition, the content of this entry is not intended for any jurisdiction outside which ShadowFall is not authorised.

This entry is for informational purposes only and is not an offer or solicitation to buy or sell any investment product. This entry is the property of ShadowFall.

ShadowFall does not take responsibility or accept any liability for any action taken or not taken by the Recipients of this entry as a result of information and/or opinions contained in the entry. Specifically, Recipients of this entry agree to hold harmless ShadowFall and its affiliates and related parties, including, but not limited to any partners, principals, officers, directors, employees, members, clients, investors, consultants and agents (collectively, the “ShadowFall Related Persons”) for any direct or indirect losses (including trading losses) attributable to any information and content on the ShadowFall website including any publications on the website.

In no event shall ShadowFall or any ShadowFall Related Persons be liable for any claims, losses, costs or damages of any kind, including direct, indirect, punitive, exemplary, incidental, special or, consequential damages, arising out of or in any way connected with any information or content on the ShadowFall website or in this entry.

Recipients must exercise their own judgment and where appropriate take their own investment, tax and legal advice prior to taking or not taking action in reliance on the contents of this entry.

Forward-looking information or statements in this entry may contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. ShadowFall makes no representation herein that forward-looking predictions shall come to pass. ShadowFall is committed to providing services and products which are unbiased and impartial and have implemented a Conflicts of Interest Policy pursuant to FCA rules.

PREPARING FOR THE WORST. HOPING FOR THE BEST.

In the halcyon days before Covid-19, when corporates were awash with credit, margins were fat, and valuations were high, issuers could run their balance sheets thinner than the tiniest of little thin wafer-thin mints. Surplus cash generation (or as was all too often proceeds of debt) could be directed either towards management pay-outs, M&A, chunky dividends, share buy backs, or all four. These days, economic activity runs cold. If you’re not in isolation under house arrest then you’re likely one of the valiant members of our society, working in healthcare to save the sick, or providing vital services such as delivering goods to those that need it.

CORPORATE STOCKPILING

How long this will continue, no one really knows. Yet, management of some companies have, in our view, taken the principled and probably sensible decision to plan for a long siege. Take for example, Hays Plc (HAS LN), the global specialist recruitment firm. Hays has been in business for as long as we can remember. Its management has decided they want that to continue. They’ve seen recessions before. They understand how devastating economic downturns can be to the top line. In recessions almost no one hires, and so recruiters’ profits generally collapse. Even if companies wanted to hire, who could when the central office is boarded up?

At the start of April, Hays took the long term – and we believe honourable – view to be straight with its investors. It decisively acted to batten down the hatches and shore up its balance sheet for what could be turbulent times ahead. It doesn’t know how long such disorderly times will last; all it knows is it wants to come out the other side.

Hays announced:

Over recent years Hays has consistently operated with a net cash balance sheet, and strongly believes this gives valuable confidence to both our clients and investors.To ensure that we have a strong balance sheet and can continue with minimal or no debt once our end markets stabilise, the Board has concluded that it is prudent to now raise equity.

This will both provide the Group with a further liquidity buffer and importantly best allow us to pursue organic growth opportunities with new and existing blue-chip clients. We are already seeing such opportunities begin to emerge and expect further vendor consolidation from our clients when markets stabilise.

Accordingly, Hays has separately announced today its intention to conduct a non-pre-emptive placing of new ordinary shares of the Company targeting gross proceeds of approximately £200 million.

Through an accelerated book build (ABB), Hays raised gross proceeds of £200 million at 95p per share. The day before the ABB its shares closed at 109.4p per share and the ABB was completed at a 13.2% discount. At the time of writing, Hays trades at 106p per share, 12% higher than the ABB price and 3% below the prior ABB close.

Another company to take the long-term view is Aviva Plc (AV/ LN), the insurance provider, in which the ShadowFall Fund holds a long position. On 8 April 2020, Aviva paid heed to the restraint urged by its regulatory authorities on dividend payments by insurers to shareholders. Aviva’s Board of Directors decided to withdraw the recommendation to pay the 2019 final dividend, which was due to be paid in June 2020.

The upshot of this was announced by Aviva as:

Aviva remains well capitalised with strong liquidity. By retaining the final dividend, the estimated group capital ratio will increase by c. 7% to approximately 182% (as of March 13, previously disclosed date.)

ST JAMES’S PLACE

ShadowFall Fund is short St James’s Place (STJ LN).

Capitalised at £4.1bn, STJ is a financial services provider, offering products in life insurance, unit trusts, pensions, and mortgage advisory.

As it happens, the ShadowFall Fund was already short STJ prior to the societal disruption caused by the spread of Covid-19. We believed that STJ was approaching a ‘pinch point’, where its management would have to choose to either use its balance sheet to prioritise the growth of its FuM or continue to provide a growing dividend. We had other concerns, but this was the most pressing. And now, in the light of the significant market moves over the past month, we believe that the risk to future dividends is the highest it has been in recent history.

SOLVENCY II

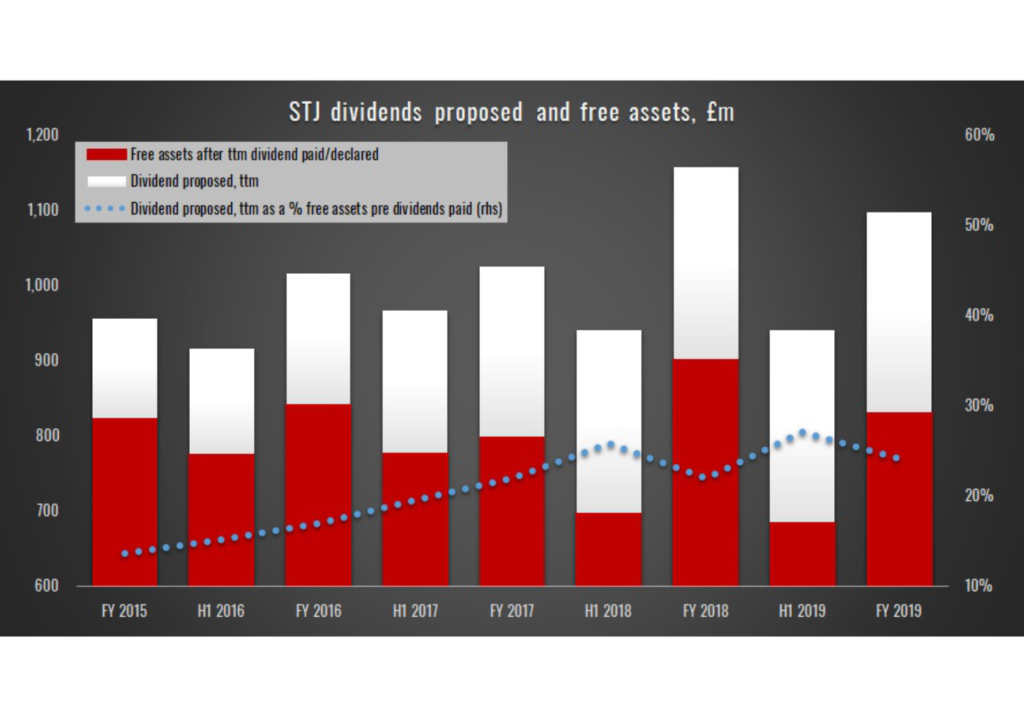

STJ highlight 2 key solvency metrics: The Solvency II free assets as well as the excess of free assets over the management solvency buffer.

As with all businesses, dividends are paid from the retained earnings generated in prior periods. Typically, the only other constraint to the dividend would be the cash available to the company. However, with Solvency II companies there is an additional constraint on the business: The Solvency II Capital Requirement (SCR). Solvency II uses a market-based approach in valuing assets, and as a result Solvency II free assets (excess assets over the SCR) can be prone to fluctuation. As such, for prudence, excess free assets are normally held over and above the minimum capital requirement.

On top of this, given that the assets on the balance sheet contribute to returns for the firm, and thus the ability to pay future dividends, management aim to extract cash in the least intrusive way on the balance sheet, so as to not cannibalise potential future growth.

When looking at the group accounts, we look at the Solvency II free assets of the group both pre and post the cash effects of dividends paid for that financial year. We believe this gives a clearer picture of the assets from which management is able to pay a dividend and normalises for seasonality between the 1H and FY payment.

We note that during the period FY15 to FY19 the trailing twelve-month (ttm) dividend has doubled to £265m, from £130m, an attractive growth rate. Over the same time period, the Solvency II free assets adding back the dividend have not really moved despite the company growing. The effect of this is that:

- The dividend as a percentage of the free assets pre dividend in 2015 was 14%, implying 7x coverage, whereas this has now risen to 24% and is now just 4x coverage.

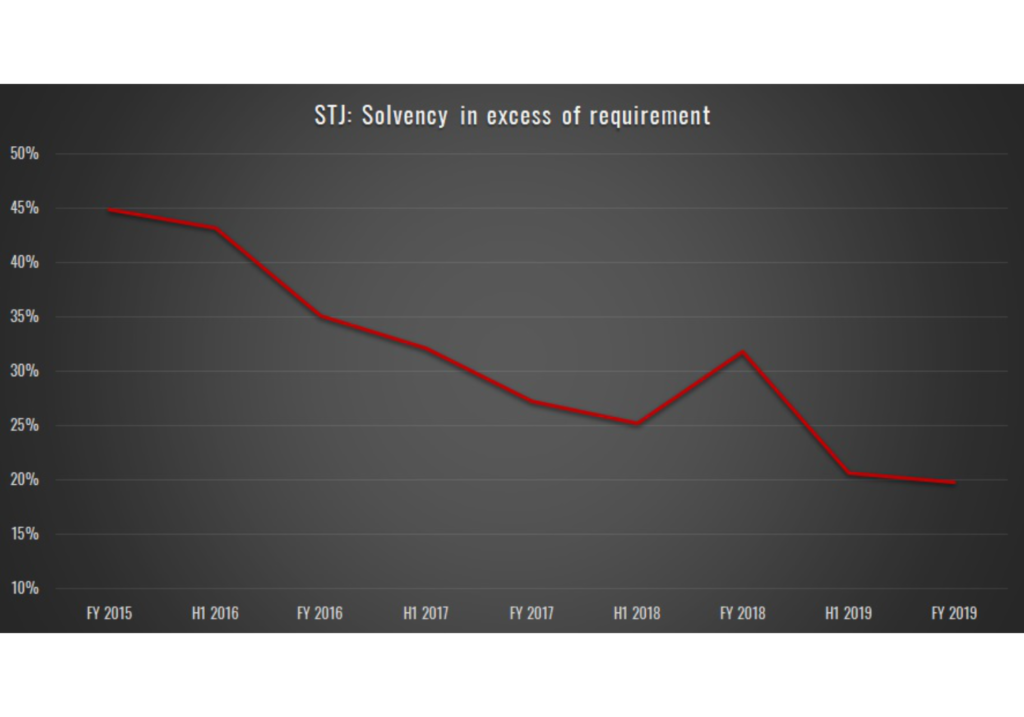

- Meanwhile, the Solvency ratio in excess of the group solvency capital requirement has deteriorated from having 45% headroom in 2015 to 20% at FY19. We believe this leaves the group more exposed to solvency risk, and the dividend’s rate of growth is currently unsustainable.

MARKET TURMOIL

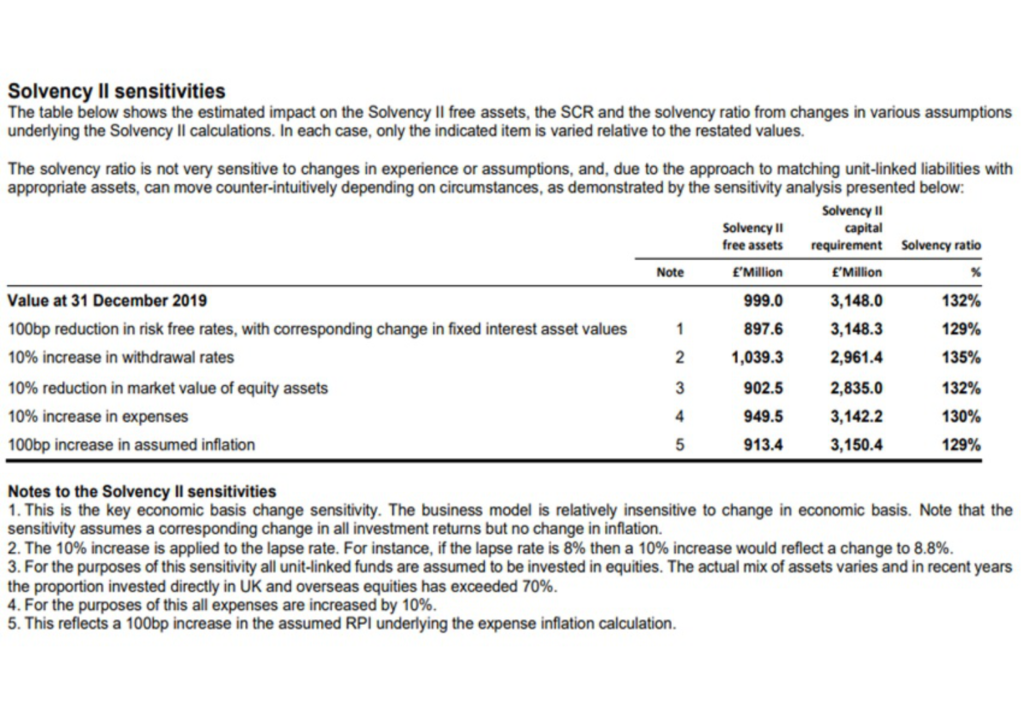

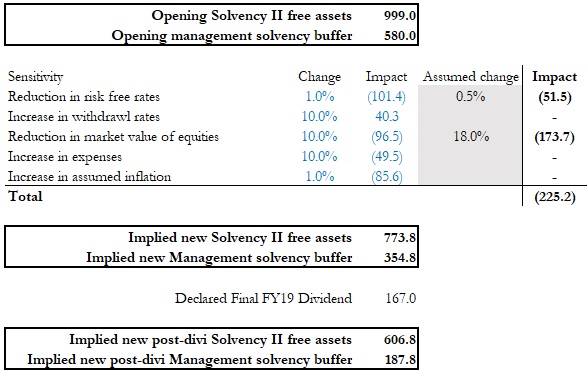

At the 2019 full year results, STJ’s management stated that Solvency II free assets (own funds less the Solvency Capital Requirement) stood at £999m and that the excess of free assets over the management solvency buffer (the Solvency II net assets less a management solvency buffer) stood at £580.6m. Both of these figures are taken pre the payment of the final dividend, which totalled a cash cost of £167m.

If we use the Solvency II sensitivity provided by management at full-year results and mark to market both of these measures for key moves in the market that we have seen year to date, we observe a significant reduction in the liquidity available to management.

STJ state that the largest equity exposures are to UK and European Equities, if we use the EURO STOXX 600 index (in GBP) as a proxy, which has fallen c. 18% YTD (as of the time of writing). The provided sensitivity implies that this would correspond to a c. -£174m drag on the Solvency II free assets, all else equal. On top of this STJ state that the risk-free rate it uses is the reference yield on ten-year gilts, YTD this has declined from 82bps to 31bps. We believe that the provided sensitivity implies that this would correspond to a c. -£52m drag on the Solvency II free assets, all else equal.

In our view, the effect of these two marks to market are a combined c. -£225m drag on the Solvency II free assets. If we adjust to include the payment of the final dividend, we calculate that it results in a total drag on Solvency II free assets since 2019-year end of c. -£392m; a reduction of c. -39%. If we assume these sensitivities also hold true for the Solvency II net asset calculation, then we calculate this puts the marked to market post-dividend excess of free assets over the management solvency buffer at just £188m; a 68% reduction since year-end 2019.

Since 2014, STJ has embarked upon a generous dividend policy paying out dividends totalling £1.07bn, against this the business has generated a “cash result” of £1.14bn. This is equivalent to an average pay-out of 94%. When it comes to the 2019 dividend, we note this pay-out rose to 116%. Management seem to us to justify the pay-out through reference to its “material flow of cash to come from our stock of gestation FUM over the medium term” (2019 financial results call). STJ’s gestation FUM refers to the FUM which STJ manages that will generate fee income in the future as and when it matures. In paying a 2019 dividend which is 16% above its cash result, we believe STJ is drawing on future cash flows to pay to shareholders today. In our view, this is a less than cautious policy. In the context of recent market moves, we question whether both STJ’s current fee earning FUM and its future FUM in gestation, will generate the fees that management had factored when it determined its dividend pre-Covid-19.

In these days of increased uncertainty, we believe it is positive when management teams make principled decisions to de-risk their respective balance sheets in order to protect the future for their stakeholders, such as in the case of Hays and Aviva. In our view these strengthening measures provide greater certainty in such turbulent times. By contrast, if companies such as STJ, in our view, flirt with Solvency II headroom in order to make generous payments to shareholders, we believe that this could store up risk issues down the road as we continue through these unprecedented times.