Published: 13th January 2020 – 14:15pm

Contact: [email protected]

Terms & Conditions:

ShadowFall Publications Limited’s terms and conditions (collectively, these “Terms”) are available here on the ShadowFall website (www.ShadowFall.com) and set out the basis on which you may make use of the ShadowFall website and its content, whether as a visitor to the ShadowFall website or a registered user. Please read these Terms carefully before you start to use the ShadowFall website.

By using, downloading from, or viewing material on the ShadowFall website you indicate that you accept these Terms and that you agree to abide by them. If you do not agree to these Terms, you must not use the ShadowFall website nor any of its content.

You must not communicate the contents of this website blog entry (“entry”) and other materials on this website to any other person unless that person has agreed to be bound by these Terms. If you access this website, download or receive the contents of website blog entries or other materials on this website as an agent for any other person, you are binding your principal to these same terms.

Disclaimer and Disclosures:

This entry, which contains an implicit recommendation, has been produced by ShadowFall Publications Limited which is an Appointed Representative (FRN 842414) of ShadowFall Capital & Research LLP which is authorised and regulated by the Financial Conduct Authority in the United Kingdom (FRN 782080) (together “ShadowFall”) and published onto the ShadowFall website (www.ShadowFall.com) on 13th January 2020.

Any information which could be construed as investment research has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is also not subject to any prohibition on dealing ahead of the dissemination of investment research.

Unless otherwise specified, the information and opinions presented or contained in this entry are provided as of the date of this entry. ShadowFall is under no obligation to update, revise or affirm this entry.

ShadowFall Capital & Research LLP manages an alternative investment fund (the “fund”) which inter alia takes positions in traded securities. At the time of publication on the ShadowFall website on 13th January 2020 , the fund holds a short position in the issuer, which may include through options, swaps or other derivatives relating to the issuer. The fund may take further positions in the issuer (long or short) at a future date. In addition, at the time of publication on the website, an author of this entry is invested in the fund.

Neither the authors nor ShadowFall are aware of any factor, subject to the paragraph above, which might reasonably be expected to impair their objectivity in the preparation of this entry. The authors and ShadowFall are not aware of any direct or indirect conflicts of interest, subject to the paragraph above, that might exist between the authors or ShadowFall and any issuer which is the subject of this entry (the “issuers”). In particular, neither the author nor ShadowFall has any affiliation with the issuers.

ShadowFall has taken all reasonable steps to ensure that factual information in this entry is true and accurate. However, where such factual information is derived from publicly available sources ShadowFall has relied on the accuracy of those sources.

Some of the open source data contained in this entry may have been sourced from public records made available by Companies House, which is licensed under the Open Government License; https://www.nationalarchives.gov.uk/doc/open-government-licence/version/3/

All statements of opinion contained in the entry are based on ShadowFall’s own assessment based on information available to it. That information may not be complete or exhaustive. No representation is made, or warranty given as to the accuracy, completeness, achievability or reasonableness of such statements of opinion.

This entry is only intended for investors who qualify as FCA defined Professional Clients (the “Recipient(s)”), who are expected to make their own judgment as to any reliance that they place on the content of the entry. This entry is not suitable for, nor intended for any persons deemed to be a “Retail Client” under the FCA Rules. In addition, the content of this entry is not intended for any jurisdiction outside which ShadowFall is not authorised.

This entry is for informational purposes only and is not an offer or solicitation to buy or sell any investment product. This entry is the property of ShadowFall.

ShadowFall does not take responsibility or accept any liability for any action taken or not taken by the Recipient of this entry as a result of information and/or opinions contained in the entry. Specifically, Recipients of this entry agree to hold harmless ShadowFall and its affiliates and related parties, including, but not limited to any partners, principals, officers, directors, employees, members, clients, investors, consultants and agents (collectively, the “ShadowFall Related Persons”) for any direct or indirect losses (including trading losses) attributable to any information and content on the ShadowFall website including any publications on the website.

In no event shall ShadowFall or any ShadowFall Related Persons be liable for any claims, losses, costs or damages of any kind, including direct, indirect, punitive, exemplary, incidental, special or, consequential damages, arising out of or in any way connected with any information or content on the ShadowFall website or in this entry.

Recipients must exercise their own judgment and where appropriate take their own investment, tax and legal advice prior to taking or not taking action in reliance on the contents of this entry.

Forward-looking information or statements in this entry may contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. ShadowFall makes no representation herein that forward-looking predictions shall come to pass. ShadowFall is committed to providing services and products which are unbiased and impartial and have implemented a Conflicts of Interest Policy pursuant to FCA rules.

BRAVADO BUYS AND UNREMITTING SALES

BRAVADO – NOUN: A BOLD MANNER OR A SHOW OF BOLDNESS INTENDED TO IMPRESS OR INTIMIDATE.

Within the arsenal of perfunctory responses typically used by the management of a company which is subject to some criticism is the “Bravado Buy”. The thinking goes that there can be no better sign than a CEO or other head honcho parting with their hard-earned cash to buy stock. If any bearish assessment had been warranted, then why would someone so close to the coalface risk losing their money? However, context is everything. A Bravado Buy is a stock purchase that may well be sizeable but relative to prior sales, it’s a fraction of the monies already banked. Take Burford Capital Limited (Burford) as a recent example.

A CASE IN POINT

On the day of the release of a short report by Muddy Waters Research (Muddy Waters), Burford’s management waved their cheque books in the air, and waded into the market to hoover up stock (our bold for emphasis):

7 August 2019

REPORT’S CRITICISMS WITHOUT MERIT AND BURFORD PRINCIPALS TO PURCHASE SHARES

The Board of Burford Capital Limited (“Burford” or the “Company”) takes note of the short attack report issued this morning by Muddy Waters, a firm known for such tactics, and believes that the report’s criticisms are without merit. Burford will issue a detailed response to the report as soon as practicable and, following that detailed response, will also convene an investor conference call, as to which participation details will be provided in due course.

Christopher Bogart and Jonathan Molot, Burford’s Chief Executive Officer and Chief Investment Officer, respectively, have informed the Board that once Burford’s detailed response to the Muddy Waters’ report allegations has been published, they each intend to purchase Burford shares for their personal accounts.

On 8 August 2019 it was announced that Mr Bogart and Mr Molot had purchased 123,747 and 350,643 shares in Burford respectively at a price of GBP 663.7 a share. A cool £821,395 bought by Mr Bogart and £2,327,463 snapped up by Mr Molot. By 12 August 2019, Mr Molot had purchased a further 339,963 shares in Burford, bringing his total purchases to £5,237,546. Many of Burford’s shareholders and its sell-side cheerleaders were positively purring.

A year or so earlier and the transactions were the other way round and considerably larger. On 20 March 2018, Burford announced that Mr Bogart and Mr Molot had sold 4.4 million and 4.3 million shares in Burford respectively, at a price of GBP 1350. Mr Bogart would have realised proceeds of £59.4 million and Mr Molot proceeds of £58.1 million.

Figure 1 Burford Capital Limited share price and insider share transactions. Source: ShadowFall, Bloomberg Finance L.P.

Post the Muddy Waters report, Mr Bogart’s purchase value of Burford shares totalled a relatively paltry 1.4% of his prior sale, while Mr Molot’s purchase equated to 9% of his prior sale. We view this as a textbook Bravado Buy. As it happens, Messrs Bogart’s and Molot’s March 2018 share disposals look to be textbook sales. Coming up to two years after these sales, Burford’s stock value is some 50% lower. Sizeable stock disposals by management are something we keep an eye out for at ShadowFall.

THE UNREMITTING SALES: SHOW ME THE MONEY! …

Figure 2 Tom Cruise from the film Jerry Maguire. Photograph: Colombia Tristar. Alamy Stock Photo

ShadowFall Fund is short Temenos AG (Temenos, TEMN SW).

In recent years, we’ve seen very few management stock disposal initiatives as regular and sizeable as those that have been chalked up by Temenos.

Temenos is a CHF 11.1bn (US$10.7bn) Swiss based provider of banking software systems for financial institutions. Its main revenues are from Software Licenses (c. 41%), SaaS (c. 4%), Software Maintenance (c. 37%) and Consulting Services (c. 18%).

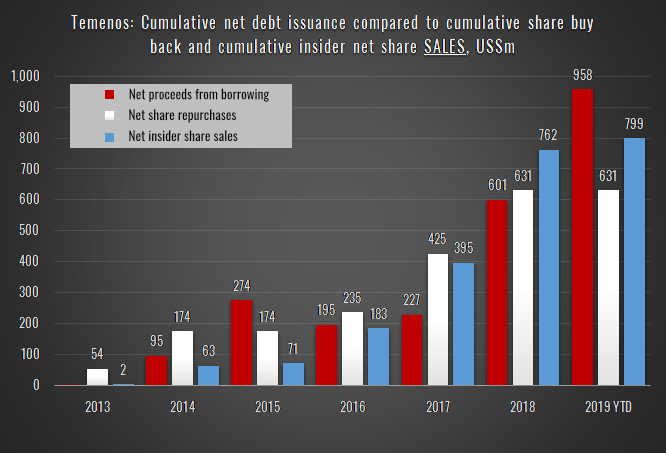

We believe that the scale of “cashing in” by Temenos’ management is eye-watering. Since 2013, we calculate that Temenos’ executives have between them sold US$809.5 MILLION in Temenos shares[1]. This compares to a relatively meagre US$10.7m in share purchases.

At the same time as these US$809.5m in executive sales have been occurring, Temenos’ management instructed the company to buy-back US$630.6m in Temenos stock. If one is happy to overlook the incongruous nature of this, where on the one hand Temenos’ management is happy for the company to buy-back stock whilst at the same time is content to personally sell stock at similar prices, then we have a few other accounting concerns regarding this arrangement.

Figure 3 Temenos Executive Director sale and purchase of Temenos shares. Source: Bloomberg Finance L.P.

Figure 4 Temenos cumulative net debt issuance, share buy backs and insider sales. Source: ShadowFall, Bloomberg Finance L.P., Temenos financial statements

SARs ATTACKS!

Figure 5 Jack Nicholson from the film Mars Attacks. Photograph: PictureLux, The Hollywood Archive. Alamy Stock Photo

The majority of Temenos’ managements’ share rewards has been issued through its Share Appreciation Rights (SARs) programme. Through this programme, we believe that Temenos:

- Is facing a future liability of at least c. US$546m on its SARs which remain outstanding.

- Is effectively “short its own shares”.

- Manages to shield significant employee associated costs/incentive plans from its P&L.

- Improves its operating and free cash flow as well as conversion, since:

a. Any P&L SARs related charge is non-cash in nature and already reduced. Hence, not only is its IFRS EBIT improved (because the cost is low and spread out) but operating cash generation is also increased.

b. But also its adjusted EBIT is improved as the cost of issuance is an adjustment – we also highlight that this measure is also a vesting criteria for the SARs.

c. To date these incentive costs are effectively absorbed within its finance cash flow section and largely sterilised under the form of share repurchases, which are then pledged to employees to settle the SARs. - Receives a higher tax expense to the disadvantage of its shareholders than would otherwise be received if the cost of the SARs arrangement was fully absorbed through its P&L.

- Although regularly highlighting its share buyback policy as accretive to shareholders, it is fairly fruitless in terms of EPS accretion, since Temenos’ share count doesn’t really decline.

WHAT DO WE WANT? “SHARE APPRECIATION RIGHTS!”

WHEN DO WE SELL THEM? “NOW!”

Figure 6 Strikers crossing London Bridge, c. 1910. Photograph: Niday Picture Library, Alamy Stock Photo.

Temenos’ SARs are granted to its executive board members and selected employees. The SARs are conditional on the employee completing a specified period of service and are only exercisable if the Group achieves specified non-IFRS earnings per share targets. In case of over achievement of earnings per share targets, certain SAR grants may be increased by a maximum of 40% of the original grant and seemingly at the original strike price, so that they are in the money at grant. The vesting period for the SARs is a minimum of three years and the SARs have a maximum contractual term of ten years.

SARs are beneficial to an employee when the company’s share price rises. Employees do not pay the exercise price but receive the sum of the increase in stock or cash. However, Temenos states that it has no legal or constructive obligation to repurchase or settle the SARs in cash. Any dilution or cash cost relating to an outstanding SAR is only known at the time of exercise as it is dependent on the share price at that time. In case of change of control in Temenos, all outstanding SARs will become immediately vested and exercisable.

As an example, if 1,000 SARs at a grant price of US$44 are exercised when the share price is US$130, then the gain is US$86,000, equivalent to a 662 share dilution.

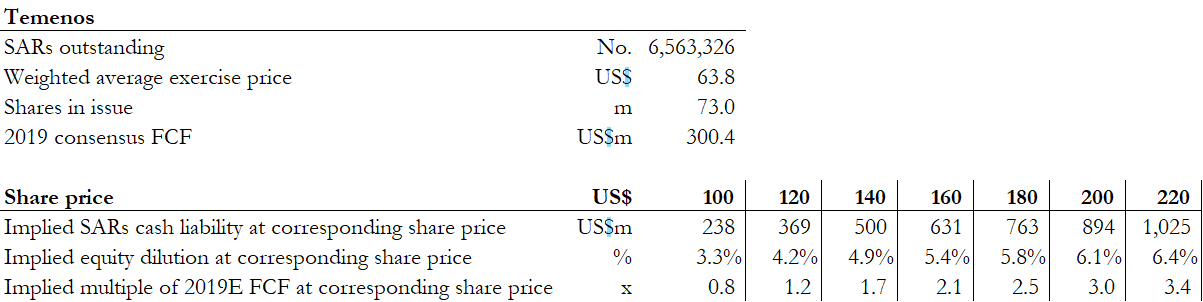

THE US$546 MILLION SARS LIABILITY

At year end 2018 (we await the update for 2019), Temenos had 6,563,326 SARs outstanding with a weighted average exercise price of US$63.8 per share. At its current share price of US$147 per share, we calculate the Group has a future liability of c. US$546m which it will need to fund via cash or equity issuance to settle. The irony is that if Temenos’ share price continues to rise, it becomes more costly to settle these SARs – hence us viewing this as Temenos being “short its own shares”.

For example:

Temenos currently trades on 39x its consensus forecast 2019 Free Cash Flow (FCF) of US$300m. This would imply for every US$10m of incremental FCF above consensus which Temenos can generate, that its market capitalisation would rise by c. US$390m, or alternatively by c. US$5.2 per share.

Since Temenos has 6,563,326 SARs outstanding we calculate that a price increase of US$5.2 per Temenos share would therefore lead to increasing its SARs liability by US$34.2m. I.e. at its current valuation, for an additional US$10m in FCF generation, it costs Temenos an extra $34.2m in cash or the equivalent equity issuance as a result. Ceteris paribus, we calculate that the only way Temenos can match such a FCF increase to the resulting increase in the SARs liability, is if incremental FCF was valued at 11x 2019 FCF.

Another way of looking at the costs associated with the outstanding SARs is through either the cash or equity issuance implications that might result from movements in Temenos’s share price. This impact is demonstrated in figure 7 below.

For example:

With 6,563,326 SARs outstanding with a weighted average exercise price of US$63.8 per share, if Temenos’s share price averages, say US$180 per share, when these SARs are exercised, then we calculate that the cash cost associated with this would be US$763m. Temenos would have the option to either settle this liability in:

- Cash, which would equate to 2.5x its 2019 consensus forecast FCF; or

- Equity, where at the same US$180 per share, would equate to the issuance of c. 4.2m shares, or 5.8% dilution. Which if true to form, we assume would be promptly liquidated by management. So much for the last few years of share buy-backs!

Figure 7 Equity or cash implications from SARs related share price scenarios. Source: ShadowFall, Bloomberg Finance L.P., Temenos financial statements.

SIGNIFICANT EMPLOYEE ASSOCIATED COSTS ARE SHIELDED FROM THE P&L

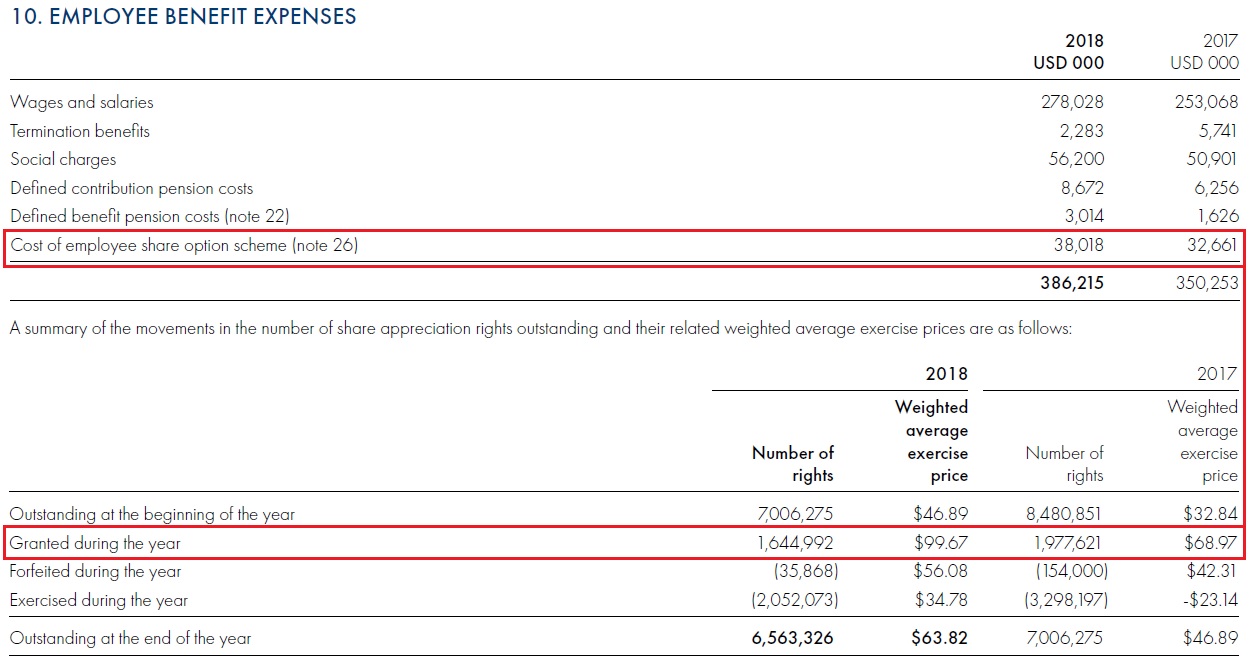

Among the accounting issues resulting from the SARs scheme is the fact that through it, Temenos manages to shield significant employee associated costs/incentive plans from its P&L.

For example:

In 2017, 1.9m SARs were granted at a US$69 exercise price for a P&L cost of US$33m. However, at its current valuation, we calculate that this will cost Temenos shareholders either a cash cost of US$154m or an equity dilution of c. 1.4% to satisfy upon the SARs being exercised.

In 2018, 1.6m SARs were granted at a US$100 exercise price for a P&L cost of US$38m. However, at its current valuation, we calculate that this will cost Temenos shareholders either a cash cost of US$77m or an equity dilution of c. 1.1% to satisfy upon the SARs being exercised.

What this means is that in just the two years of 2017-18, at its current valuation, either a cash cost of US$231m or an equity dilution of c. 3.5% is waiting to be absorbed by Temenos’ shareholders for a P&L cost of just US$71m.

Figure 8 Temenos employee performance incentive costs. Source: ShadowFall, Temenos financial statements.

SIGNIFICANT EMPLOYEE ASSOCIATED COSTS ARE SHIELDED FROM OPERATING AND FREE CASH FLOW

In addition to the P&L shelter, the manner in which the SARs have been settled means that the associated costs are largely shielded from its operating section and passed through the company’s financing section of its cash flow statement.

For example:

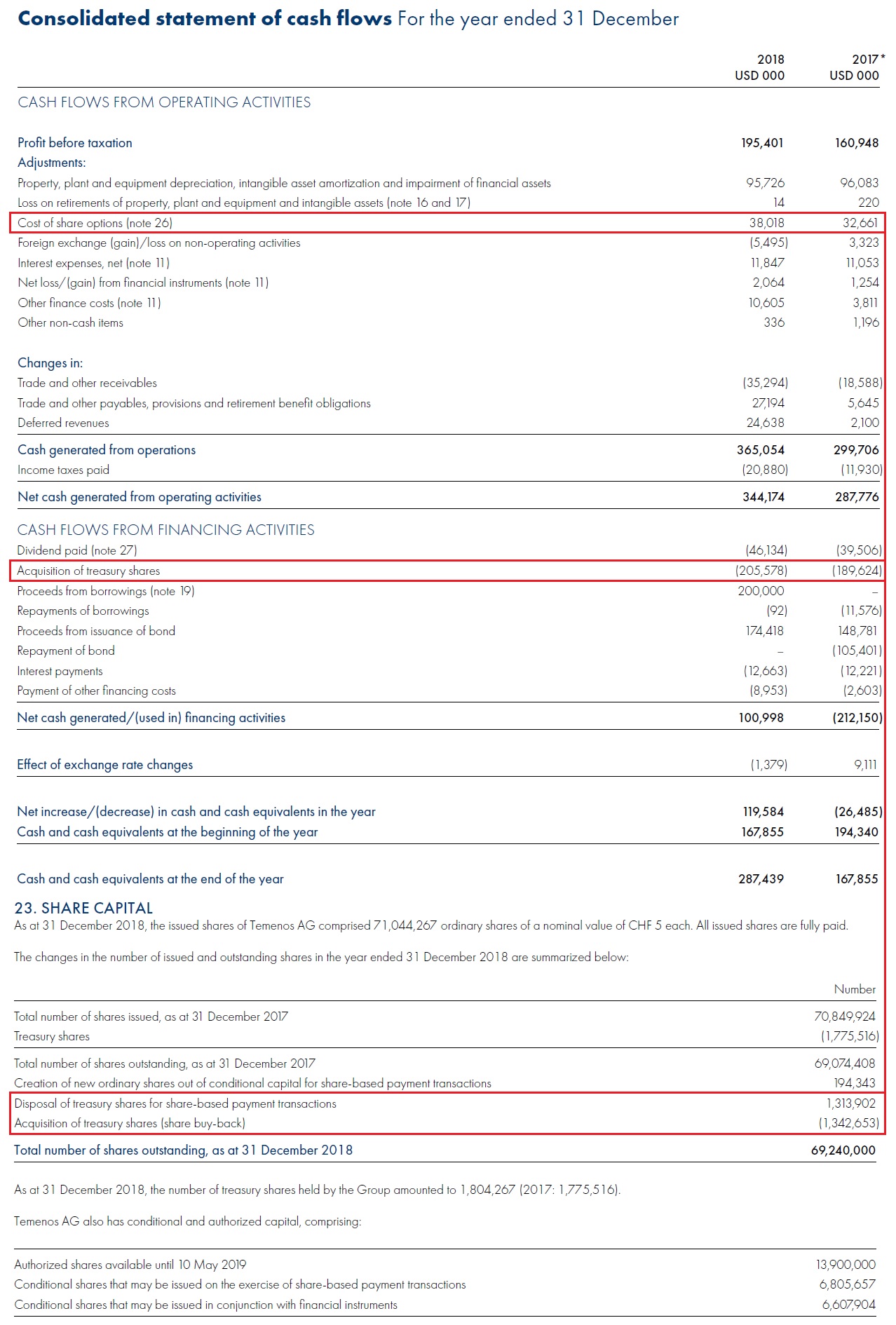

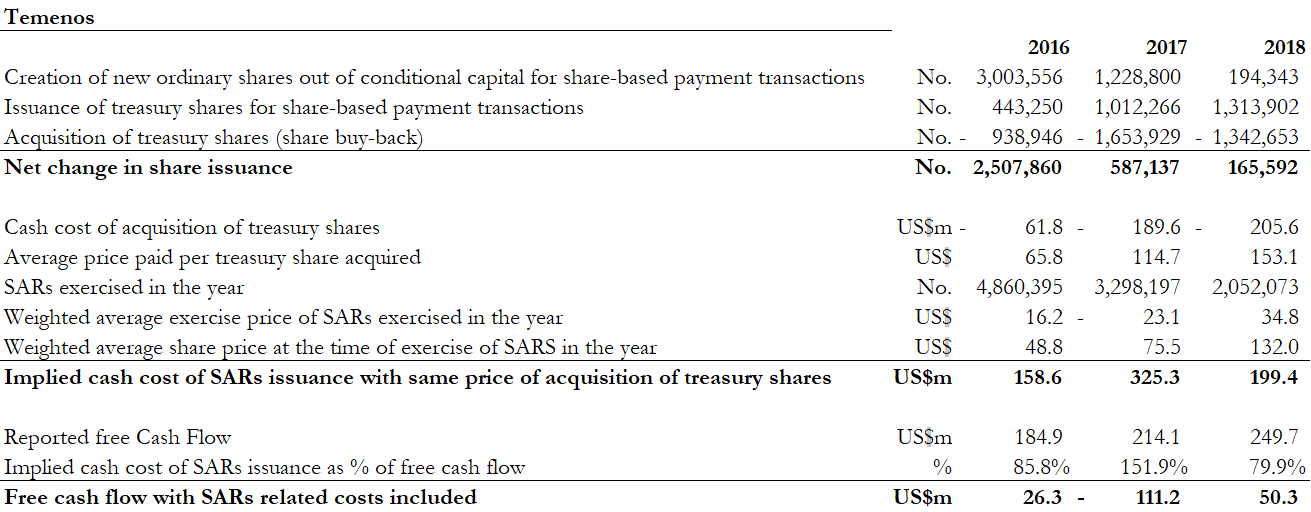

While the relatively modest cost of US$33m and US$38m in relation to share options were added back though the operating section of the cash flow statement for 2017 and 2018 respectively, further down in the financing section, the considerable cost of former SARs issuance is clear. Temenos spent US$190m and US$206m on acquisition of treasury shares in 2017 and 2018 respectively. In actual share terms this translated into 1,653,929 and 1,342,653 shares repurchased into treasury in 2017 and 2018 respectively. However, in order to settle share-based payment transactions, 2,241,066 and 1,536,996 in shares were either created or disposed of in 2017 and 2018 respectively, i.e. the SARs related costs from issuance in earlier years.

Effectively, what shares were bought back in the market by Temenos and costed through the financing section of its cash flow, were then handed back to its management in SARs related liabilities in order for management to then sell these into the market.

Figure 9 Temenos employee performance incentive costs & financing of share buyback & share issuance. Source: ShadowFall, Temenos financial statements.

RUNNING OUT OF ROAD?

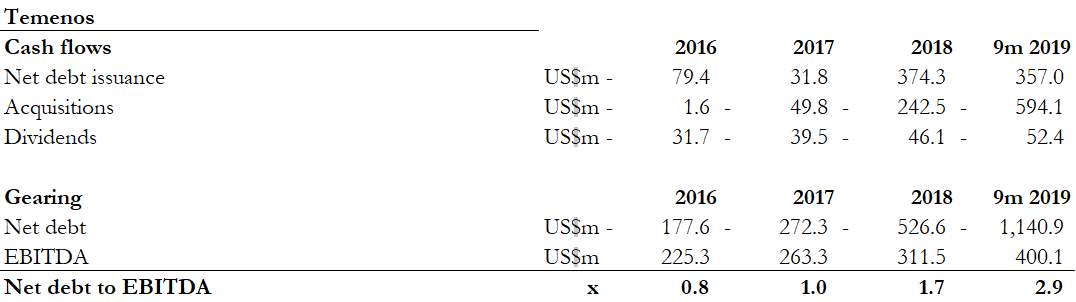

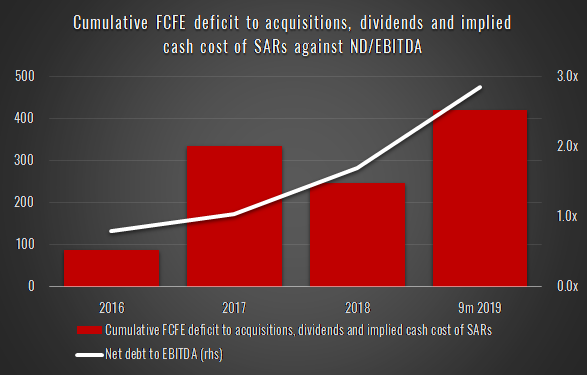

One can argue that the sizeable share buy-backs of recent years have either been funded by Temenos’s free cash flow or increased net debt issuance. As we highlight above and provide in more detail in figure 10 below, we believe that free cash flow has been strengthened due to the SARs awards and the way that they are accounted for in the group’s cash flow statement. Meanwhile, net debt has risen significantly, from US$225m in 2016, to US$1,141m by 30 September 2019. As such, net debt to 2019 consensus EBITDA has risen from 0.8x in 2016 to 2.9x by 30 September 2019, although is forecast by consensus to reduce to 2.3x by year end 2019. Either-way:

- There remain 6,563,326 SARs outstanding, not to mention any further SARs that will have been issued in 2019 and may be in the years ahead; and

- The group is guiding to deleverage.

It appears to us that if free cash flow is going to be used to deleverage, then Temenos’ shareholders will need to factor in a reversal of the prior years’ buy-backs as shares are issued to management to settle the SARs as they are exercised.

Or,

If free cash flow is used to settle to the SARs in cash terms, then the sizeable nature of these awards will become more apparent to Temenos’ shareholders, who may wonder why so much of free cash flow is being directed towards this arrangement.

We believe that the most likely scenario is a reversal of the share buy-back since otherwise the group has less ability to reduce gearing and it is more overtly obvious to its shareholders how well rewarded management is.

We believe that figure 10 demonstrates this below.

For example:

In 2018, the group purchased 1,342,653 shares through its share buy-back at a total cost of US$205.6m for an average purchase price per share of US$153.1 per share. However, in the same year, it issued 1,313,902 and created 194,343 shares for share-based payment transactions; 1,508,245 combined. Hence, despite the share buy-back, Temenos’ share issuance actually increased by 165,592 shares. Further, 2,052,073 SARs were exercised in 2018 (2017: 3,298,197), at an average share price of US$131.96 per share (2017: minus US$23.14 per share ). These were sold at a weighted average price at the time of exercise of US$131.96 per share (2017: US$75.49 per share) meaning that if these had been settled in cash it would have cost Temenos US$199.4m (2017: US$325.3m).

Note: we also find it interesting that management exercised their SARs at an average of US$131.96 per share in 2018 (2017: US$75.49 per share), when the buy-back cost an average of US$153.1 per share in 2018 (2017: US$114.7 per share). I.e. the company paid an average of US$39.2 and US$21.1 per share higher for its buy-back shares in 2017 and 2018 respectively than the level at which Temenos’ management were willing to sell.

The cash value of the SARs exercised in 2018 totalled US$199.4m (2017: US$325.3m), which compares to FCF of US$249.7m in 2018 (2017: US$214.1m). As we have detailed above, these employee-related costs/incentives are shielded from the group’s FCF. If the SARs related costs had been settled by way of cash as opposed to equity and included in free cash flow, then the group would have reported US$50.3m in FCF in 2018 (2017: MINUS US$111.2m), currently valuing Temenos at a 253x EV to 2018 FCF! As it happens they were actually settled by way of share issuance, which was somewhat sterilised by the share buy-back programme.

Figure 10 SARs implications, EBITDA 2019 = FY Bloomberg consensus forecast. Source: ShadowFall, Bloomberg Finance L.P., Temenos financial statements.

Figure 11 Cash flows and expenditures (US$m) and net debt to EBITDA (x), EBITDA 2019 = FY Bloomberg consensus forecast. Source: ShadowFall, Bloomberg Finance L.P., Temenos financial statements.

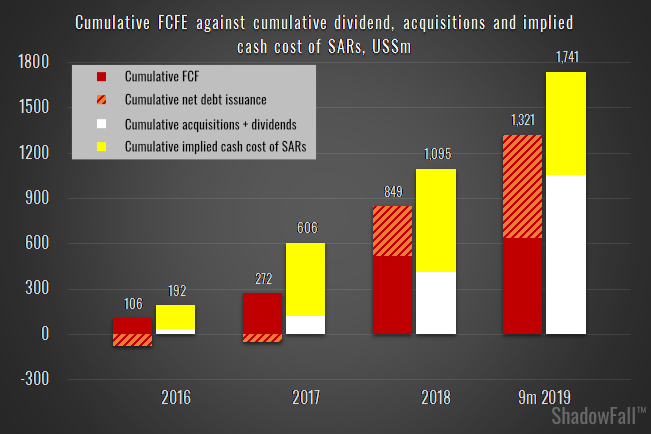

Figure 12 Cumulative FCFE against cumulative dividend, acquisitions and implied cash cost of SARs, Source: ShadowFall, Temenos financial statements

Figure 13 Cumulative FCFE deficit to acquisitions, dividends and implied cash cost of SARs against net debt to EBITDA (x), EBITDA 2019 = FY Bloomberg consensus forecast. Source: ShadowFall, Bloomberg Finance L.P., Temenos financial statements.

WHY HAS TEMENOS PLEDGED ITS ENTIRE STOCK OF TREASURY SHARES TO BANQUE HAVILLAND?

Figure 14 “Banque Havilland”, Luxembourg. Photograph: Maurice Savage, Alamy Stock Photo

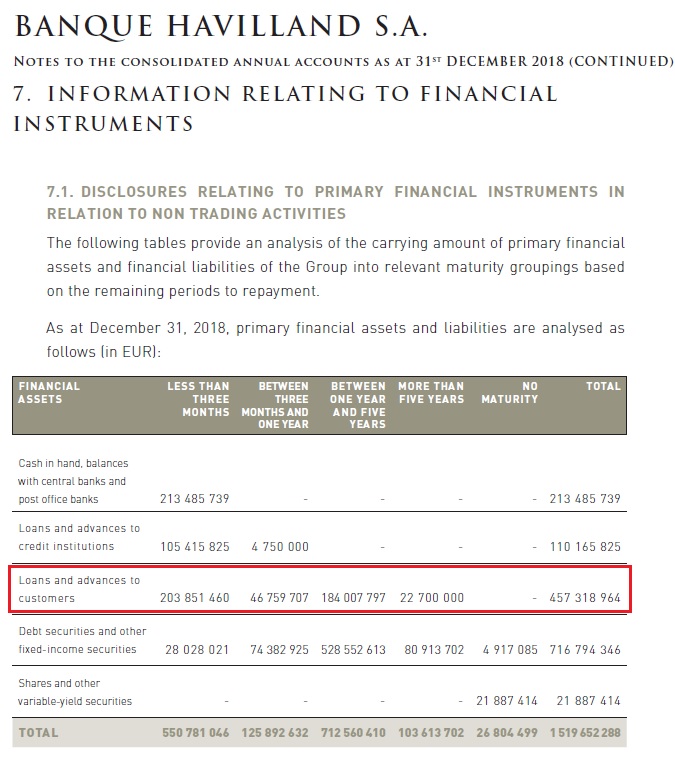

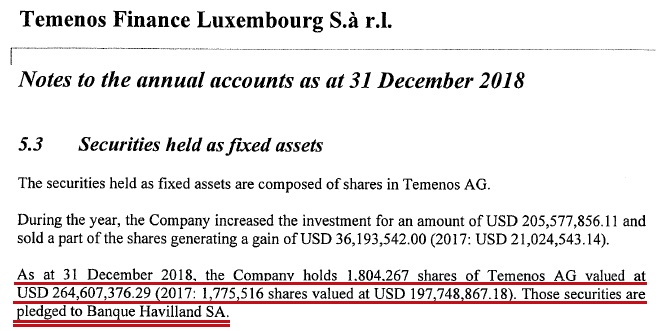

SARs liabilities aside, what we find somewhat odd is that when it comes to Temenos’ treasury stock, we discover that this has been pledged to a relatively small, independent and privately owned bank, Banque Havilland. We are unable to find disclosure of this arrangement in Temenos’ consolidated group accounts, but rather we have to refer to the accounts of its Luxembourg subsidiary, Temenos Finance Luxembourg S.à.r.l.

At 31 December 2018, Banque Havilland reports loans and advances to customers of €457m or US$524m. What we find odd is that according to Temenos Finance Luxembourg’s 2018 filing, Temenos had pledged its entire stock of 1,804,267 Treasury shares, with a value of US$265m, to Banque Havilland. Temenos’ Treasury shares were also pledged to Banque Havilland in 2017 and 2016.

Figure 15 Banque Havilland financial assets as of 31 December 2018. Source: ShadowFall, Banque Havilland filings.

Typically, when a person or entity pledges stock it is as collateral. It’s possible that this arrangement in some way relates to servicing the SARs programme. Nonetheless, we believe that this arrangement could warrant greater disclosure than effectively being tucked away in a Luxembourg subsidiary’s filings. Especially given the significant size of the nominal value of the stock pledged and the fact it seemingly relates to Temenos’ entire stock of treasury shares.

Alternatively, if it’s unrelated to the SARs then it raises further obvious questions such as:

- Is it another form of financing that Temenos is using above its existing debt facilities?

- What value did Temenos receive against US$265m of pledged stock?

- If it is an equity related loan, what happens if the value of Temenos’ shares decline?

Figure 16 Temenos Finance Luxembourg S.à.r.l. 2018 financial statements. Source: ShadowFall, Temenos Finance Luxembourg S.à.r.l.

IN SUMMARY

As a conclusion, we believe that Temenos’ SARs arrangement to reward its employees enables it to flatter its P&L, operating and free cash flow. The fact that these share awards appear to be sold almost as soon as they become eligible to exercise doesn’t inspire us with great confidence. Going forward, if the group is to de-lever, then it seems likely to us that the scale and cost of these awards will become more apparent to Temenos’ shareholders. However, these are not the only risks that we have identified.

[1] Source: Bloomberg Finance L.P. calculated as number of shares multiplied by the closing share price

[2] Source: Bloomberg

[3] Of course, this works in reverse, in that if consensus FCF declines by US$10m, then its SARs liability reduces by US$34.2m. Since we have a short position in Temenos, this would be acceptable.

[4] consensus of US$274.7m + US$10m

[5] We note that the 2017 SARs are reported to have been exercised with a negative exercise price of minus US$23.14. At first we thought this might be a typo but it is reported in the 2017 and 2018 accounts. It is unclear to us how a share can be issued with a negative price.