Terms & Conditions:

ShadowFall Publications Limited’s terms and conditions (collectively, these “Terms”) are available here on the ShadowFall website (www.ShadowFall.com) and set out the basis on which you may make use of the ShadowFall website and its content, whether as a visitor to the ShadowFall website or a registered user. Please read these Terms carefully before you start to use the ShadowFall website.

By using, downloading from, or viewing material on the ShadowFall website you indicate that you accept these Terms and that you agree to abide by them. If you do not agree to these Terms, you must not use the ShadowFall website nor any of its content.

You must not communicate the contents of this report and other materials on this website to any other person unless that person has agreed to be bound by these Terms. If you access this website, download or receive the contents of reports or other materials on this website as an agent for any other person, you are binding your principal to these same terms.

Disclaimer and Disclosures:

This website entry (“entry”), which contains an implicit recommendation, has been produced by ShadowFall Capital & Research LLP (“ShadowFall”), which is authorised and regulated by the Financial Conduct Authority in the United Kingdom (firm reference number 782080). and published onto the ShadowFall website (www.ShadowFall.com) on 1 July 2019.

Unless otherwise specified, the information and opinions presented or contained in this entry are provided as of the date of this entry. ShadowFall is under no obligation to update, revise or affirm this entry.

ShadowFall Capital & Research LLP manages an alternative investment fund (the “fund”) which inter alia takes positions in traded securities. At the time of publication on the ShadowFall website on 1 July 2019, the fund holds a short position in the issuer, which may include through options, swaps or other derivatives relating to the issuer. The fund may take further positions in the issuer (long or short) at a future date. In addition, at the time of publication on the website, an author of this entry is invested in the fund.

Neither the authors nor ShadowFall are aware of any factor, subject to the paragraph above, which might reasonably be expected to impair their objectivity in the preparation of this entry. The authors and ShadowFall are not aware of any direct or indirect conflicts of interest, subject to the paragraph above, that might exist between the authors or ShadowFall and any issuer which is the subject of this entry (the “issuers”). In particular, neither the author nor ShadowFall has any affiliation with the issuers.

Unless otherwise specified, the information and opinions presented or contained in this entry are provided as of the date noted above. ShadowFall is under no obligation to update, revise or affirm this entry.

ShadowFall has taken all reasonable steps to ensure that factual information in this entry is true and accurate. However, where such factual information is derived from publicly available sources ShadowFall has relied on the accuracy of those sources.

Some of the open source data contained in this report may have been sourced from public records made available by Companies House, which is licensed under the Open Government License; https://www.nationalarchives.gov.uk/doc/open-government-licence/version/3/

All statements of opinion contained in the entry are based on ShadowFall’s own assessment based on information available to it. That information may not be complete or exhaustive. No representation is made or warranty given as to the accuracy, completeness, achievability or reasonableness of such statements of opinion.

This entry is only intended for and will only be distributed to investors who qualify as FCA defined Professional Clients (the “Recipient(s)”), who are expected to make their own judgment as to any reliance that they place on the content of the entry. This document is not suitable for, nor intended for any persons deemed to be a “Retail Client” under the FCA Rules. In addition, the content of this entry is not intended for any jurisdiction outside which ShadowFall is not authorised.

This entry is for informational purposes only and is not an offer or solicitation to buy or sell any investment product. This report is the property of ShadowFall.

ShadowFall does not take responsibility or accept any liability for any action taken or not taken by the Recipient of this entry as a result of information and/or opinions contained in the entry. Specifically, Recipients of this entry agree to hold harmless ShadowFall and its affiliates and related parties, including, but not limited to any partners, principals, officers, directors, employees, members, clients, investors, consultants and agents (collectively, the “ShadowFall Related Persons”) for any direct or indirect losses (including trading losses) attributable to any information and content on the ShadowFall website including any publications on the website.

In no event shall ShadowFall or any ShadowFall Related Persons be liable for any claims, losses, costs or damages of any kind, including direct, indirect, punitive, exemplary, incidental, special or, consequential damages, arising out of or in any way connected with any information or content on the ShadowFall website or in this entry.

Recipients must exercise their own judgment and where appropriate take their own investment, tax and legal advice prior to taking or not taking action in reliance on the contents of this entry.

Forward-looking information or statements in this entry may contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. ShadowFall makes no representation herein that forward-looking predictions shall come to pass. ShadowFall is committed to providing services and products which are unbiased and impartial and have implemented a Conflicts of Interest Policy pursuant to FCA rules.

The existence and content of this entry have not been discussed in any way with the issuers or their corporate brokers prior to completion and publication. Neither the authors nor ShadowFall has received any payment from the issuer, its corporate broker or any connected party for preparing this entry.

Prior to completion and distribution, this entry has been seen by ShadowFall’s legal advisers and its regulatory advisers.

TALK ABOUT CLOSENESS? WE’VE NEVER HAD IT SO GOOD.

The Financial Times’ journalists, Madison Marriage and Jonathan Ford, wrote a compelling report in August 2018: A dangerous dance – when auditors are too close to the client. Ms Marriage and Mr Ford highlight the plights of a former auditor at PwC, Mauro Botta, who apparently filed a case in early 2018 against PwC. Mr Bota alleged that:

Defendants [PwC et al] engaged in unlawful retaliatory employment practices prohibited by §1102.5, by terminating and otherwise retaliating against Plaintiff [Mr Botta] because Plaintiff was and is a bona fide whistleblower; Plaintiff objected to unlawful practices, as promulgated by Federal Law, SEC regulations, SEC Administrative Guidance, and industry standards; Plaintiff refused to participate in fraudulent, negligent, and inaccurate work-related-activities; Plaintiff made numerous internal complaints about perceived unlawful practices and actual unlawful practices.

In other words, Mr Botta alleged after he had highlighted what he perceived to be poor practices at PwC that PwC unlawfully fired him for doing so. To be fair to PwC, in its response to the Financial Times, PwC states that “Mr Botta’s claims are completely false. His employment was terminated for legitimate business reasons, and we will prove that in court.”

As far as we are able to deduce this case is ongoing, however, regardless of this specific case, Ms Marriage and Mr Ford go on to discuss the closeness of audit firms to their clients; a subject which has featured elsewhere [1] [2] in the press over the past year.

If we thought UK auditors can on occasion be cosy with their clients, over in France things are (as one might expect) positively romantic.

EUROFINS: KEEP YOUR FAMILY CLOSE

Eurofins Scientific S.E. (Eurofins) is a French listed, €7,106m market cap company. Eurofins started out in business in 1987, floated in 1997, and describes itself as a world leader in providing laboratory based analytical services in the testing, inspection and certification (TIC) market to the pharmaceutical, food, environmental, clinical and consumer product markets.

Eurofins’ board comprises six individuals: its founder, CEO and Chairman, Dr Gilles Martin; his brother, Dr Yves-Loic Martin; a woman who appears to be the CEO’s spouse, Valerie Anne Marie Hanote-Martin and three other individuals – talk about keeping it in the family. The Martin Family currently holds 36% of Eurofins’ shares through a Luxembourg entity, Analytical Bioventures SCA, and retains 56.6% of the voting shares.

Eurofins reported revenue of €3.78bn and net income of €356m to 31 December 2018.

KEEP YOUR AUDITOR CLOSER?

We take our hat off to PwC, Eurofins’ auditor of at least 18 years, for Eurofins has what we view as a complicated and seemingly ever-changing structure.

In Eurofins’ 2017 financial statements the Group reports “more than 35,000 staff in a network of companies operating in more than 400 laboratories across 44 countries.” A year later, in 2018, the Group cites “more than 45,000 staff” operating in “more than 800 laboratories”. Seemingly gaining 10,000 more staff and twice as many laboratories within the space of one year.

In 2017, Eurofins made c. 60 acquisitions and in 2018, it purchased c. 50 businesses. Evidently the Group buys businesses at an average rate of one per week; an impressive figure for any management team.

When it comes to subsidiaries, we count around 560 in 2016, rising to over 700 in 2017, and by 2018 approaching 800.

Until April 2019, PwC was lined up to audit Eurofins’ accounts for at least the 19th consecutive year. Initially, in its draft AGM resolutions statement from 25 March 2019, Eurofins notified that it planned to renew the mandate for PwC for its 2019 financial year. A few weeks later, on 10 April 2019, Eurofins amended its AGM resolution to state that it planned to appoint Deloitte as its auditor for its 2019 financials. When questioned about the seemingly sudden change of plan for PwC’s reappointment on its 26 April 2019 conference call, Dr Gilles Martin stated:

“And as to the auditor, we started a call for offer with different auditors and it just took a little bit too long to finalize it. So it wasn’t finished, the call for offer when we sent the invitation for the annual meeting. We’re quite happy with PwC. We have no complaints. The only reason we changed is that apparently some market participants thought that we have been too long with PwC, I don’t think so. But frankly, if that’s what it takes to make people happy, we change, there’s no problem.”

A LUX ROMANCE?

While the annulment of PwC’s appointment is of some interest, seemingly a fair amount of the heavy lifting for historical audit work has been performed by a relatively small audit firm based in Luxembourg: Audit Conseil Services S.à.r.l. (ACSe). Huh??? No, neither have we.

ACSe reported c. €1.3m in revenue in 2018 (2017: €1.1m) and employs 14 persons.

A Belgian based auditor, Vandelanotte, is another firm which historically has audited a number of Eurofins’ Belgian based subsidiaries. ACSe and Vandelanotte audited the 2017 financial statements for what appear to be Eurofins’ two largest subsidiaries: Eurofins International Holdings Lux S.à.r.l and Eurofins GSC Finance NV. We calculate that c. 79% of Eurofins’ assets reside within these two entities.

ACSe and Vandelanotte appear to have overlap in ownership.

Whilst auditing the majority of Eurofins’ Luxembourg and Belgian based subsidiaries in 2017, ACSe and Vandelanotte also appear to have audited the private entities of Eurofins’ CEO and Chairman, Dr Gilles Martin. Such entities include Analytical Bioventures SCA (36% shareholder of Eurofins), and International Assets Finance S.à.r.l, the latter being the entity through which the Martin family holds control over a number of subsidiaries that own the real estate which is leased back to Eurofins.

With ACSe booking €1.3m in revenue in 2018, Eurofins and its CEO’s private companies would seem to have been sizeable clients for ACSe. We calculate from disclosures in the respective company filings that the combined audit work performed for Eurofins and its CEO likely represented at least 8% of ACSe’s total revenue in 2018. We reckon that this could easily be a minimum.

TIL DEATH TEMPORARY BANS DO US PART?

When it comes to signing the audit reports of the Luxembourg and some of the Belgian entities, we find that an individual by the name of Erik Snauwaert was the principal signee for 2017. Mr Snauwaert was apparently subject to “a temporary ban to sign statutory audit reports” for twelve months by the Commission de Surveillance du Secteur Financier (CSSF) in March 2017. In our view, this all seems a bit odd. To be fair to Mr Snauwaert, when questioned in a telephone interview by Bloomberg’s, David Hellier, (Eurofins won’t use Auditor who also worked for CEO’s firm March 6, 2019) Mr Snauwaert apparently:

‘… confirmed the one-year ban but said it didn’t prevent him from undertaking client audit work that wasn’t governed by Luxembourg law. He declined to comment on the reason for the ban. Neither he nor his firm were the overall auditor of the company, he said, and the Eurofins entities reviewed by his firm were sub-holding companies, not operational ones.’

We view this as a bit disingenuous, as for example, Eurofins Forensics Lux Holding (a subsidiary of Eurofins) received its 2016 audit signed by Mr Snauwaert on 20 April 2017. This was less than 30 days AFTER his temporary ban was apparently implemented. According to Eurofins Forensics Lux Holding’s 2016 financial statements, Mr Snauwaert signed beneath an opinion as follows:

Opinion

A notre avis, les Comptes Annuels donnent une image fidèle du patrimoine et de la situation financière de Eurofins Forensics LUX Holding Sàrl au 31.12.2016, ainsi que des résultats pour l’exercice clos à cette date, conformément aux obligations légales et réglementaires relatives à l’établissement et la présentation des Comptes Annuels en vigueur au Luxembourg.

THIS TRANSLATES AS FOLLOWS:

Opinion

In our opinion, the Annual Accounts give a true and fair view of the assets and financial position of Eurofins Forensics LUX Holding Sàrl as at 31.12.2016, as well as the results for the financial year ended on that date, in accordance with the legal and regulatory requirements relating to the preparation and presentation of the Annual Accounts in force in Luxembourg.

As highlighted above, this opinion was signed by Mr Snauwaert less than thirty days AFTER his temporary ban AND appears to be in accordance with the legal and regulatory requirements in force in Luxembourg. If this doesn’t mean governed by Luxembourg law then we don’t know what does. Mr Snauwaert went on to sign Eurofins Forensics Lux Holdings’ 2017 financial statements on 26 April 2018.

We wrote a letter to Mr Snauwaert on June 4, 2019, (receipt signed June 11, 2019). Our letter highlighted this apparent contradictory statement attributable to him, stating that we would be grateful if he could provide a specific explanation as to why he was able to issue his opinion in accordance with the legal and regulatory requirements in force in Luxembourg whilst under a ban by the CSSF. At present, we have not received a response from Mr Snauwaert.

Aside from the end of PwC’s term for auditing the Group accounts, we believe a more relevant question is if it will be the end of ACSe and Vandelanotte’s involvement in Eurofins’ subsidiary audit work?

AND JUST ONE MORE THING (FOR NOW) …

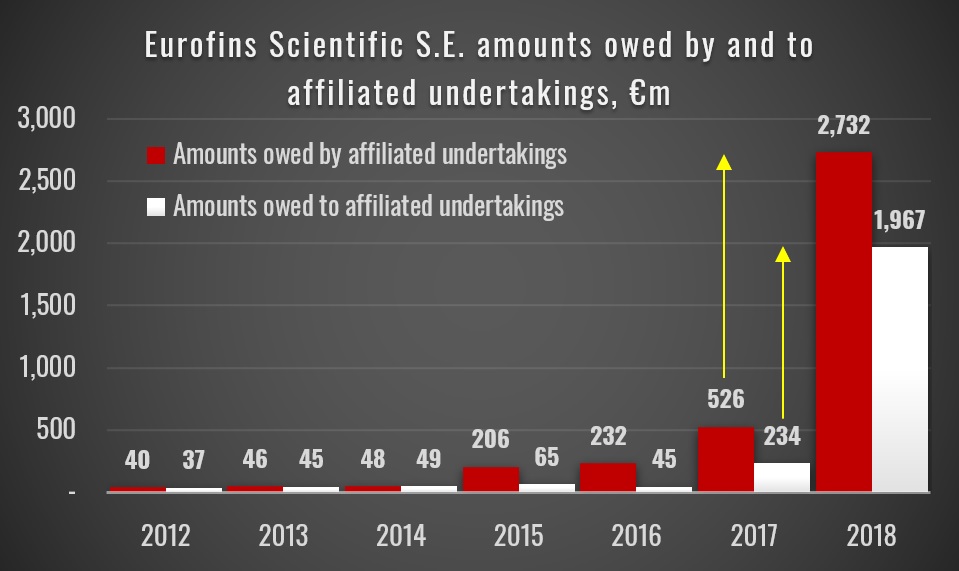

Whilst on the subsidiaries, we couldn’t help but notice that according to Eurofins’ 2018 financial statements, Eurofins Scientific S.E. (the top co) advanced €2,732m to its affiliated undertakings in 2018. This was an increase of €2,207m owed to it by subsidiaries from the €526m it advanced in 2017. Meanwhile, Eurofins Scientific S.E. (the top co) owed €1,967m to its undertakings in 2018; an increase of €1,733m it owes to its subsidiaries from the €234m it owed in 2017.

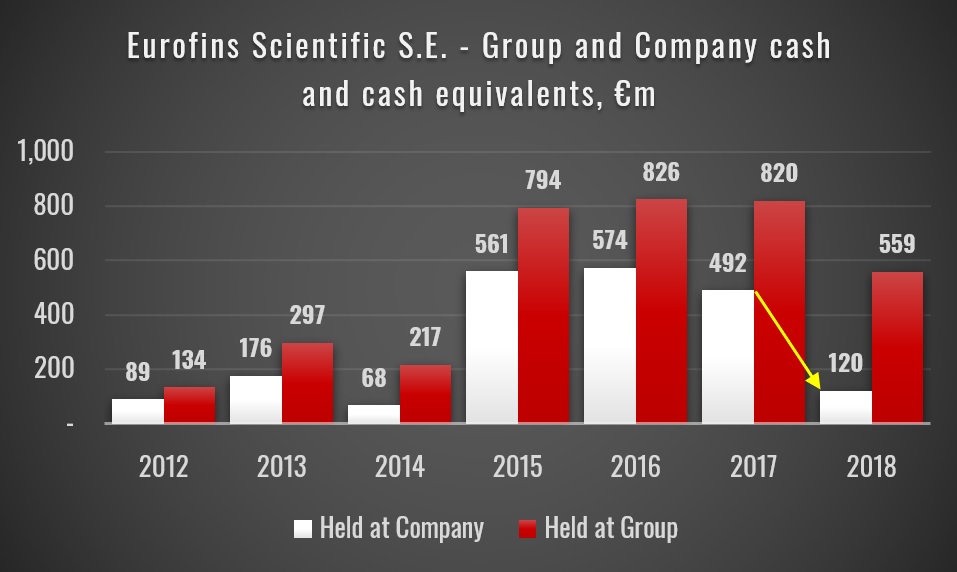

Further, whereas Eurofins Scientific S.E apparently held €492m of its total €820m in cash at bank and in hand in 2017, by 2018 this had declined to €120m of its total €559m balance at a Group level. Seemingly Eurofins is holding increasing amounts of its cash at a subsidiary level and is owed and owes significantly more by and to its subsidiaries.

In the light of what we view as a complex structure as detailed above, we believe Eurofins’ new auditor certainly has its work cut out.